BY CHRIS MILLAS

THIS DOCUMENT WILL UPDATE AUTOMATICALLY WITH NEW REVISIONS

NOT FINANCIAL ADVICE

READ MY INVESTMENT THESIS ON BITCOIN HERE

MICROSTRATEGY ONE-PAGER SUMMARY

PROFILE

COMPANY | TICKER | CATEGORY |

MicroStrategy | $MSTR | Finance |

THE BUSINESS

MicroStrategy is the largest publicly traded analyst software company in the world that is transitioning to becoming the largest publicly traded Bitcoin Treasury Company in the world that buys and holds Bitcoin as a reserve asset and leverages it to preserve and grow shareholder value.

THE MANAGEMENT TEAM

Michael Saylor founded MicroStrategy in 1989 and has steered the company through the fast-evolving technological landscape. He is a unique visionary with skin in the game and has the understanding and commitment necessary to successfully pursue a Bitcoin strategy.

THE FINANCIALS & KPI’S

Between 2023 and 2024, MicroStrategy increased its Bitcoin Per Share by 86.90%.

THE OPPORTUNITIES

- Visionary leader with skin in the game.

- Corporate monopoly on Bitcoin.

- Bitcoin Yield.

- Positioned to become the largest global Bitcoin Bank.

- New FASB rules adoption will allow MicroStrategy to report its Bitcoin holdings at fair value.

- Future S&P 500 index inclusion will accelerate and strengthen Bitcoin flywheel.

THE RISKS

- Bitcoin Extinction Event

- Prolonged Decline In Bitcoin Price

CONCLUSION

Through its ability to leverage capital markets combined with being positioned to become the largest global Bitcoin Bank, MicroStrategy continues to provide a way for investors to significantly outperform alternative Bitcoin investment vehicles.

FULL ANALYSIS

THE BUSINESS

MICROSTRATEGY

WHAT IS MICROSTRATEGY?

MicroStrategy is the largest publicly traded analyst software company in the world that is transitioning to become the largest publicly traded Bitcoin Treasury Company in the world.

A BRIEF HISTORY

MicroStrategy was founded in 1989 by Michael Saylor as a business intelligence (BI) software provider, helping organisations analyse their data and make informed decisions.

MicroStrategy went public in 1998 on NASDAQ, capitalising on the growing demand for data analytics during the dot-com boom.

In 2000, MicroStrategy faced significant challenges due to accounting issues, leading to restated financials and a sharp decline in its stock price. Despite this setback, the company rebuilt its reputation over the next two decades, solidifying its position as a leader in BI. It expanded its platform to include mobile and cloud-based analytics, serving enterprise customers worldwide.

In 2020, driven by concerns over inflation and declining fiat currency value, MicroStrategy pivoted from its traditional focus on BI to adopt Bitcoin as its primary treasury reserve asset, transforming its identity into a hybrid Bitcoin and software business.

In parallel, Michael Saylor transitioned to Executive Chairman to focus on MicroStrategy’s Bitcoin strategy, while Phong Le took over as CEO to manage the core BI business.

IS THE BUSINESS SIMPLE OR COMPLEX?

The best ideas are often the simplest (Occam’s Razor).

The price of stock correlates inversely with the thickness of its research file. The thickest files are the most troublesome and will fall the furthest. The thinnest files are the least troublesome and will rise the furthest (Sosnoff's Law).

- Simple

INDUSTRY

WHAT INDUSTRY IS THE BUSINESS IN?

- Business Intelligence (Software Side)

- Financial Services (Bitcoin Treasury Company Side)

NARRATIVES

Narrative epidemics can be fast or slow, big or small. Narrative constellations have more impact than any one narrative. The economic impact of narratives may change through time. Changing details matter as narratives evolve over time. Truth is not enough to stop false narratives — Truth matters, but only if it is in-your-face obvious. Contagion of economic narratives builds on opportunities for repetition. Reinforcement matters. Economic narratives thrive on human interest, identity and patriotism.

WHAT IS THE BUSINESS’ LONG-TERM NARRATIVE?

The narrative will evolve over time.

MicroStrategy is a corporate monopoly on Bitcoin and digital capital.

The only MicroStrategy elevator pitch you’ll ever need:

MicroStrategy is the largest corporate holder of the hardest ever commodity in the biggest global asset class.

“I want to own dominant technology monopolies that everybody needs, nobody understands and are unstoppable.” — Saylor

IS THE NARRATIVE CLEAR, SIMPLE, CREDIBLE, AUTHENTIC & EMOTIONAL?

Good business storytellers must understand their business, their audiences and themselves and must craft clear, simple stories that reflect reality.

- Resoundingly so.

ON A SCALE OF 1-10, HOW CONTANGIOUS IS ITS LONG-TERM NARRATIVE?

- 9.5

IS THE CURRENT NARRATIVE AROUND THE BUSINESS BEING DRIVEN BY INTERNAL OR EXTERNAL FORCES? IF INTERNALLY, IS THE NARRATIVE BEING BACKED UP BY RESULTS & DATA?

- Internal. Resoundingly so.

BUSINESS MODEL

WHAT IS THE BUSINESS’ BUSINESS MODEL?

MicroStrategy’s business model is to buy, hold and leverage Bitcoin to grow corporate value.

MOAT

Companies with an enduring moat protect their “above average” returns for longer.

"When you encounter these truths that other people don't understand, you just have to latch on to them big-time…Anytime you get a truth that humanity doesn't understand, that's a huge competitive advantage.” — Pabrai

WHAT COMPETITIVE ADVANTAGES DOES THE BUSINESS HAVE?

- Cult

- First Mover Advantage

- Flywheel

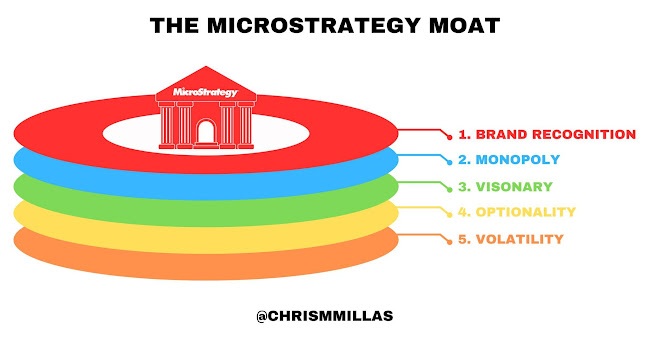

WHAT FORMS THE BUSINESS’ ECONOMIC MOAT?

- Brand Recognition

- Monopoly

- Optionality

- Visionary

- Volatility

IS THE MOAT WIDENING OR NARROWING?

- Widening.

FLYWHEELS

LEVERAGING CAPITAL MARKETS

MicroStrategy’s strategic use of capital markets fuels a reflexive flywheel.

- The more capital is raises, the more Bitcoin it can buy.

- The more Bitcoin it buys, the more the price of Bitcoin increases.

- The more the price of Bitcoin increases, the bigger its market cap.

- The bigger its market cap, the more capital it can raise.

- Repeat.

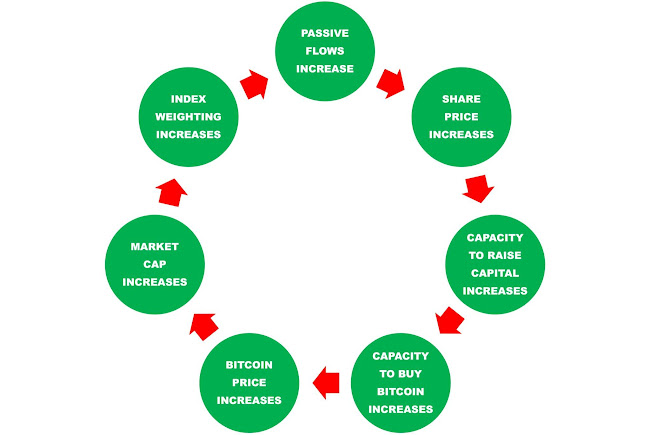

MARKET INDEXES

MicroStrategy stands to benefit disproportionately from index inclusion due to a reflexive flywheel.

- The more passive flows it attracts from indexes, the higher its share price.

- The higher its share price, the more capital it can raise.

- The more capital it can raise, the more Bitcoin it can buy.

- The more Bitcoin it buys, the more the price of Bitcoin increases.

- The more the price of Bitcoin increases, the bigger its market cap.

- The bigger its market cap, the bigger the weighting in indexes.

- The bigger the weighting in indexes, the more passive flows it attracts.

- Repeat.

MicroStrategy doesn’t need indexes. Indexes need MicroStrategy.

MONOPOLY

In the context of bitcoin holdings, MicroStrategy likely has a monopoly because there are very few companies that have the realistic potential to either match or surpass them for a number of reasons.

Firstly, there are very few companies that have the capital or financial leverage required to purchase such a large amount of bitcoin.

Secondly, of the companies that do have the capital or financial leverage required, they don’t have CEO’s with the understanding, passion and commitment — as exemplified by Michael Saylor — required to aggressively and successfully pursue a bitcoin strategy.

Thirdly, of the companies that do have the capital or financial leverage and do have CEOs with the understanding, passion and commitment required, they don’t have the ownership structure that would allow the CEO to unilaterally pursue a bitcoin strategy without broader shareholder approval — unlike MicroStrategy and Michael Saylor, who holds over 50% of voting rights.

Fourthly, even if all the aforementioned criteria are satisfied and another corporate entity does attempt to surpass MicroStrategy's bitcoin holdings, their demand would drive up the price of bitcoin which, as a byproduct, would increase the market cap of MicroStrategy and provide an opportunity for it to raise even more capital and further increase its bitcoin holdings.

Fifthly, smaller companies are behind and cannot scale the Bitcoin strategy the way MicroStrategy can while larger companies have a core business and cannot offer pure-play bitcoin exposure the way MicroStrategy can.

Sixthly, Bitcoin's volatility deters most corporations because it introduces financial unpredictability, complicating cash flow management and risk assessment.

“Here’s the reality, MicroStrategy is the most compelling story in corporate finance.” — Dylan LeClair

MENTAL MODELS

WHAT MENTAL MODELS ARE RELEVANT, EITHER FOR OR AGAINST?

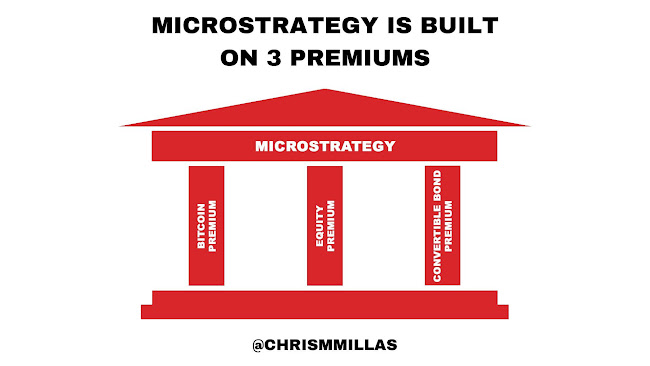

- MicroStrategy Leverages 3 Premiums

- Bitcoin Premium

- Equity Premium

- Convertible Bond Premium

All 3 premiums create and fuel each other.

It’s also important to note that MicroStrategy can issue convertible bonds at a premium even when trading at 1x mNAV. This in and of itself justifies and reinforces a higher mNAV, which creates a positive feedback loop.

- MicroStrategy Is The Amazon Of Fixed Income

The same way Amazon became the go-to for consumer products at scale is the same way that MicroStrategy is becoming the go-to for financial products at scale.

MicroStrategy is an idea whose time has come.

- MicroStrategy Is The Standard Oil Of Bitcoin

The same way Rockefeller aggregated standardised crude oil as an energy resource, MicroStrategy is aggregating and standardising Bitcoin as a financial resource.

The same way Standard Oil redefined the energy industry, MicroStrategy is redefining the financial industry.

Today, it is impossible to imagine life without oil. Tomorrow, it will be impossible to imagine life without Bitcoin.

- MicroStrategy Is The McDonald’s Of Digital Property

The same way that McDonald’s acquires and leverages physical real estate is the same way that MicroStrategy acquires and leverages digital real estate.

- MicroStrategy Is A Transformer

MicroStrategy is a transformer that converts Bitcoin volatility into tailored risk-reward profiles to suit the unique goals of different baskets of investors.

- MicroStrategy Is Leading The Digital Transformation Of Energy

MicroStrategy is leading the digital transformation of energy by capturing low frequency energy from the analogue world — fiat — that is decreasing in value and transmuting it into high frequency energy in the digital world — Bitcoin — that is decreasing in value.

MicroStrategy aggregates and leverages impure fiat and transmutes it into pure Bitcoin.

"It's not a money glitch. It's a digital transformation of the capital markets.” — Michael Saylor

- MicroStrategy Is The Next Digital Monopoly

Amazon monopolised digital commerce. Apple monopolised digital devices. Google monopolised digital information. Facebook monopolised digital relationships. Netflix monopolised digital entertainment. Spotify monopolised digital music. MicroStrategy is monopolising digital capital.

Bitcoin facilitated the transition to digital capital. MicroStrategy is accelerating the transition to digital capital.

- MicroStrategy Is The New Hurdle Rate

MicroStrategy is the new minimum rate of return that investors must consider when evaluating alternative investment opportunities.

- MicroStrategy Is Securitising Bitcoin

MicroStrategy is securitising Bitcoin by creating financial products that allow investors to gain indirect exposure to the asset eliminating the need to directly purchase, hold or manage the asset itself.

MicroStrategy is wrapping a commodity as a security.

“MicroStrategy has made a strategic decision to securitize bitcoin as an asset class. We will live or die based on bitcoin." —Michael Saylor

- MicroStrategy Is The Bridge Between TradFi & Bitcoin

MicroStrategy is capturing — and is the most efficient and effective alternative vehicle for — capital that is either restricted from (because of regulations) or reluctant to (because of volatility) flow directly into Bitcoin. MicroStrategy then converts this capital into Bitcoin, removing supply forever.

Bitcoin bridges the gap between the physical realm and the digital realm. MicroStrategy bridges the gap between Bitcoin and TradFi.

MicroStrategy creates financial instruments with different levels of volatility, performance and risk to suit different types of investors.

- MicroStrategy Is The Bridge To A Bitcoin Standard

MicroStrategy is spearheading the global shift to a Bitcoin standard, paving the way for widespread adoption and guiding the transition.

“MicroStrategy is the vehicle by which the entire world transitions to a Bitcoin standard. They're building the road and then driving the world down the road to full Bitcoin adoption.” — @PunterJeff

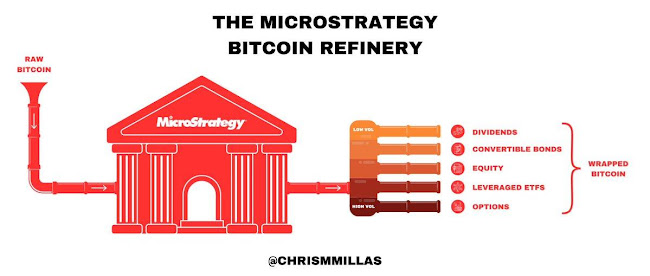

- MicroStrategy Is Wrapped Bitcoin

MicroStrategy acts like wrapped Bitcoin by creating financial products that provide investors with indirect exposure to the asset eliminating the need to directly purchase, hold or manage the asset itself. Investors can customise their exposure based on their risk tolerance and return goals.

- MicroStrategy Is Both Long Global Carry & Short Global Carry

MicroStrategy benefits from both buying Bitcoin during times of loose monetary conditions (long global carry) and holding Bitcoin during times of tight monetary conditions (short global carry).

Consequently, it’s able to profit from two seemingly opposing financial strategies at once.

“MicroStrategy is the only trade in the world that is both short global carry and long global carry.” Jeff Parks

- Endgame

The endgame for MicroStrategy is to become the biggest global Bitcoin Bank, providing financial products and services backed by Bitcoin.

“The endgame is to be the leading Bitcoin Bank, or merchant bank, or you could call it a bitcoin finance company.” — Michael Saylor

- Tipping Point

All forms of progress (momentum) happen gradually then suddenly.

When Bitcoin adoption reaches tipping point, its price will increase exponentially and so too will MicroStrategy.

- Lindy Effect

The Lindy Effect describes robustness. The longer something has survived, the longer its likely to survive. The longer something hasn't happened, the less likely it will happen.

MicroStrategy’s current operating history of 35 years suggests its likely continue surviving long into the future.

- Sosnoff’s Law

The price of a stock correlates inversely with the thickness of its research file. The thickest files are the most troublesome and will fall the furthest. The thinnest files are the least troublesome and will rise the furthest (Sosnoff's Law).

MicroStrategy satisfies Sosnoff’s Law because its investment thesis is simple: 1, leverage capital markets to maximise Bitcoin holdings and 2, leverage Bitcoin holdings to maximise cash flows.

- Volatility Is A Feature, Not A Bug — MicroStrategy Profits From Volatility

MicroStrategy issues convertible bonds to raise cash, which it then uses to buy Bitcoin.

These bonds are attractive because they offer investors the potential to convert them into MicroStrategy shares which are tethered to Bitcoin's performance.

By doing this, MicroStrategy effectively "sells volatility.” While investors benefit from Bitcoin's potential upside through the bonds' conversion feature, MicroStrategy benefits from the capital raised to increase its Bitcoin holdings.

Volatility is vitality. Reflexivity is the lifeblood.

“The volatility is the price you pay in order to create billions of dollars of credit and liquidity at your fingertips all times, everywhere, for everybody.” — Michael Saylor

- Zipf’s Law

Zipf’s law states that in many systems, the largest item is approximately twice the size of the second-largest, three times the size of the third-largest and so on.

For example, in language, the most frequent word in a text occurs approximately twice as often as the second most frequent word, three times as often as the third and so on.

If we apply this law to Bitcoin, MicroStrategy is will likely end up holding twice as much Bitcoin as the second-largest corporate holder, three times as much Bitcoin as the third largest corporate holder etc.

- MicroStrategy Benefits From Both Moves Up & Moves Down

MicroStrategy is the only stock where shareholders can celebrate — and benefit from — both moves up and moves down in price.

When the price moves up, shareholders benefit from the increased value of MicroStrategy’s Bitcoin holdings, increasing share price.

When the price moves down, shareholders benefit from equity that MicroStrategy can issue at lower prices to buy more Bitcoin, increasing Bitcoin Per Share.

Volatility, both to the upside and to the downside, also makes MicroStrategy bonds more attractive.

KPI’S

WHAT ARE THE MOST IMPORTANT KPI’S FOR MEASURING THE SUCCESS OF THE COMPANY?

- Bitcoin Yield

- Bitcoin Per Share

- Total Bitcoin Holdings

BITCOIN YIELD

WHAT IS BITCOIN YIELD?

Bitcoin Yield is defined as the % change period-to-period between Bitcoin holdings and Assumed Diluted Shares Outstanding.

HOW IS BITCOIN YIELD CALCULATED?

Bitcoin Yield = End Period Bitcoin Per Share / Start Period Bitcoin Per Share * 100

HOW IS BITCOIN YIELD GENERATED?

Bitcoin Yield is driven by accretive dilution.

MicroStrategy generates accretive dilution when the % increase in Bitcoin holdings outweighs the % increase in shares outstanding.

For example, if Bitcoin holdings increase by 10% whilst shares outstanding increases by 5%, the dilution in shares is accretive because the result is a net +5% increase in Bitcoin Yield.

BITCOIN PER SHARE

WHAT IS BITCOIN PER SHARE?

Bitcoin Per Share is defined as the Total Bitcoin Holdings relative to the Assumed Diluted Shares Outstanding.

HOW IS BITCOIN PER SHARE CALCULATED?

Bitcoin Per Share = Total Bitcoin Holdings / Assumed Diluted Shares Outstanding

When the increase in Bitcoin holdings outweighs the dilution from issuing new shares, it becomes accretive and the net Bitcoin Per Share increases.

HOW CAN MICROSTRATEGY INCREASE BITCOIN PER SHARE?

There are two ways to increase Bitcoin Yield;

- Buy Bitcoin when the stock is trading at a premium to its NAV.

- Buy back shares when the stock is trading at a discount to its NAV.

TOTAL BITCOIN HOLDINGS

WHA IS TOTAL BITCOIN HOLDINGS?

Total Bitcoin Holdings is defined as the total number of Bitcoin owned by MicroStrategy at any given point in time.

MicroStrategy is worth 2.1% of all the money in the world.

COMPETITION & MARKET SHARE

IS THE BUSINESS CLEARLY DIFFERENTIATED FROM ITS COMPETITORS?

Yes. It has a monopoly on Bitcoin.

WHO ARE THE BUSINESS’ MAIN COMPETITORS?

Within the context of Bitcoin, it has none.

THE OPPORTUNITIES

With foresight, MicroStrategy is inevitable.

BITCOIN TREASURY COMPANY

MicroStrategy is transitioning from an analytics software company into a Bitcoin Treasury Company (BTC) that buys and holds Bitcoin as a primary reserve asset and leverages it to preserve and grow shareholder value.

“We're building up a massive digital capital base that we can then lever, that will support our equity, our options, our derivatives and all the fixed income instruments we issue.” — Michael Saylor

“Our objective is to find ways to generate incremental Bitcoin for our shareholders and do that with either cash flow from the business or do it through intelligent accretive financings of equity or debt or other intelligent operations. Also, if you just buy the Bitcoin you can't generate yield.” — Michael Saylor

“Nothing is more powerful than an idea who’s time has come.”

MICROSTRATEGY VERSUS ALTERNATIVE BITCOIN INVESTMENT VEHICLES

MicroStrategy offers a unique value proposition compared to other Bitcoin investment vehicles.

- Largest Corporate Holder Of Bitcoin — MicroStrategy holds significantly more Bitcoin than any other public company.

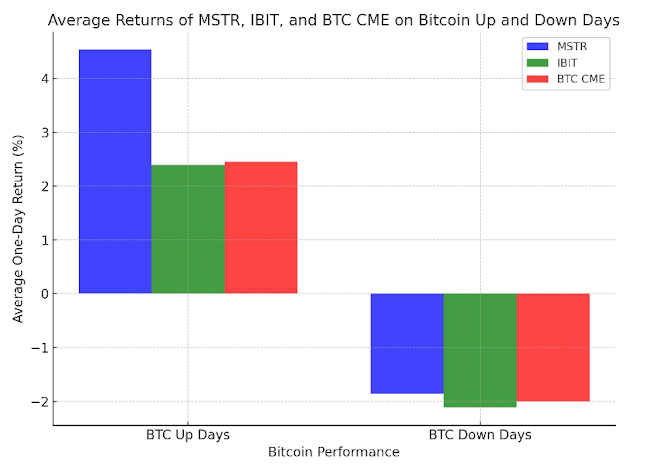

- Downside Protection —MicroStrategy outperforms ETF’s and Bitcoin Futures both on Up Days and Down Days.

- Financial Leverage — MicroStrategy uses debt to acquire bitcoin. The more the price of bitcoin increases, the more capital the company can raise to buy more bitcoin and further increase its Bitcoin Per Share, creating a flywheel effect.

- Generated Yield — MicroStrategy generates yield by leveraging cheap debt to increase its bitcoin holdings.

- No Fees — MicroStrategy provides a way for investors to gain indirect exposure to bitcoin without paying management fees.

- Accretive Dilution — MicroStrategy is actively increasing its Bitcoin Per Share (BPS) by leveraging capital markets to buy Bitcoin.

- International Gateway — MicroStrategy offers international investors indirect access to Bitcoin, enabling those who might otherwise face barriers to invest or allowing them to do so in a more tax efficient manner. For example, many overseas tax-advantaged savings plans and pension plans cannot directly invest in U.S. ETFs or purchase Bitcoin due to regulatory or other constraints. However, they can invest in NASDAQ-listed stocks.

- Deep Liquidity — MicroStrategy's stock is highly liquid, making it easier for large investors to buy and sell without significantly impacting the price.

- Deep Options Market — MicroStrategy has a deep options market due to its high volatility, strong correlation with Bitcoin and institutional interest.

- Indexes Inclusion — The more indexes MicroStrategy is added to, the more passive investment flows it attracts, the bigger its market cap, the more capital it can raise and the more Bitcoin it can purchase, creating a flywheel effect.

- Bitcoin Bank Potential — As the largest corporate holder of bitcoin, MicroStrategy is positioned to become a Bitcoin Bank by offering products and services backed by bitcoin.

Note: As highlighted below, owning shares of MicroStrategy does not entitle you to the Bitcoin that the company holds.

BITCOIN SPOT VERSUS MICROSTRATEGY STOCK

You can either buy raw (directly holding the asset through an exchange) Bitcoin or wrapped (indirectly owning the asset through an equity) Bitcoin. MicroStrategy serves investors who want wrapped Bitcoin.

First you become Orange Pilled. Then you become Red Pilled.

If you’re optimising for self sovereignty, there is no second-best to $BTC. If you’re optimising for ROI, there is no second-best to $MSTR.

People discover $BTC on a need-to-know basis. People discover $MSTR on a want-to-know basis.

$BTC is savings technology. $MSTR is compounding technology.

$BTC is for people on defense. $MSTR is for people on offense.

$BTC stores wealth. $MSTR multiplies it.

$BTC is the apex commodity. $MSTR is the apex equity.

$BTC minimises risk. $MSTR maximises returns.

$BTC is for the risk-averse. $MSTR is for the risk-seeking.

$BTC locks wealth. $MSTR unlocks wealth.

Bitcoin is Number Go Up (NGU) technology. MicroStrategy is Bitcoin Per Share Go Up (BPSGU) technology.

People discover $BTC on a need-to-know basis. People discover $MSTR on a want-to-know basis.

DOWNSIDE PROTECTION

Research produced by @btcjvs demonstrates how MicroStrategy outperforms ETF’s & Bitcoin Futures both on Up Days and Down Days.

“Owning MicroStrategy is better than owning a Bitcoin ETF.” — Bill Miller IV

LEVERAGING BALANCE SHEET & FINANCIAL MARKETS

Through its balance sheet, MicroStrategy leverages fiat money that is decreasing in value to buy Bitcoin that is increasing in value.

As the value of MicroStrategy’s Bitcoin holdings increase, so too does its capacity to leverage capital markets, creating a flywheel effect.

MicroStrategy has low exposure to fiat decay ― all other companies not leveraging bitcoin have high exposure to fiat decay.

Once you truly see what MicroStrategy is doing, you can’t unsee it.

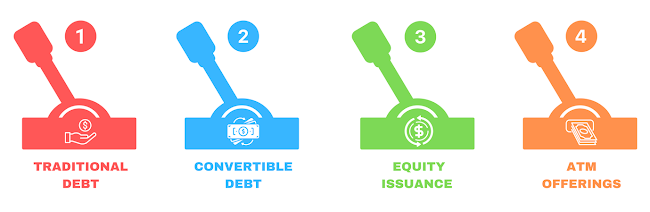

CAPITAL LEVERS

MicroStrategy has 4 main capital levers it can use to fund its Bitcoin strategy:

- Traditional Debt, which involves borrowing at fixed interest rates.

- Convertible Debt, which involves issuing debt that can be converted into shares.

- Equity Issuance, which involves selling common and preferred stock.

- At-The-Market (ATM) Offerings, which involves selling shares directly into the market.

Note: Equity issuance can target both private and public investors and involves raising a fixed amount of capital at a set price. ATM offerings are exclusively for the public market and involve selling shares gradually at real-time market prices.

“MicroStrategy is eating into the equity market, the options market, the convertible market and other markets like the fixed income market.” — Michael Saylor

“…any given time, the capital markets have opportunities and the question is, is it the fixed income market, the convert market, the preferred market or the equity market that's offering cheap capital. We will just tap any and all of them, and maybe all at the same time in sequence and then wrap that back into Bitcoin.” — Michael Saylor

SHORT INTEREST

It’s important to note that the majority of short interest is convertible bond traders hedging.

BORROWING POWER NOT LIMITED BY SOFTWARE BUSINESS

As Saylor has pointed out himself, MicroStrategy’s borrowing capacity is not limited by the earnings capacity of its software business. There are no covenants in the bonds that demand interest to be paid out of operating cash flows.

Therefore, as long as the price of Bitcoin continues to increase over time, MicroStrategy can finance its interest costs, either through debt or equity, without selling a single bitcoin.

“The more important point, there's no covenants that are geared to EBITDA. The operating business is not a limiting factor. There's no reason why we can't do $4bn in debt. Then $8bn in debt, then $16bn in debt, then $32bn, then $64bn and $128bn.” — Michael Saylor

“I don’t have any problem seeing how we could raise $100B more capital and then $200B after that.” — Michael Saylor

CONVERTIBLE BONDS

WHAT IS A CONVERTIBLE BOND?

A convertible bond is a debt instrument that that allow creditors to earn interest whilst also retaining the option to convert the debt into a predetermined number of shares at a predetermined price. Is the option is not exercised, debtors repay the debt at maturity.

Convertible bond buyers aren’t concerned with the interest feature — they are concerned with the convert feature.

HOW IS A CONVERTIBLE BOND PRICED?

Convertible bond is priced based on interest rates, credit worthiness, underlying stock price and volatility of the stock.

HOW DOES MICROSTRATEGY BENEFIT FROM VOLATILITY?

The volatility in the MicroStrategy share price is beneficial for two reasons.

The volatility to the upside benefits MicroStrategy because existing convertible bonds have the opportunity to convert to equity.

The volatility to the downside benefits MicroStrategy because they can issue new convertible bonds at lower conversion prices that are more attractive to investors.

MicroStrategy is demonetising the bond market.

KEY COMPONENTS OF CONVERTIBLE BONDS

A convertible bond is a hybrid security with 6 main elements:

- Principal: The face value repaid at maturity.

- Coupon: The fixed interest paid periodically.

- Conversion Ratio: The number of shares the bond converts into.

- Conversion Price: The share price at which conversion occurs.

- Maturity: The date when principal is repaid if not converted.

- Optionality: The holder decides whether to convert to equity.

The higher the conversion price for a given convertible bond offering, the more accretive the dilution.

Importantly, conversion removes the liability from MicroStrategy’s balance sheet.

The more bonds MicroStrategy issues and the bigger it becomes, the greater its credit quality and the better conditions that it can secure. This is all while MicroStrategy is actively contributing to the maturity of Bitcoin as an asset.

HOW CONVERTIBLE BOND ARBITRAGE WORKS (H/T @hillery_dan)

- Step 1. MicroStrategy issues a convertible bond.

- Step 2. Convert arbitrage traders buy the convertible bond using borrowed money.

- Step 3. Convertible arbitrage traders then hedge their position by shorting 70% of the bond’s value in MicroStrategy stock.

- Step 4a. If the MicroStrategy share price increases, the bond’s delta (the sensitivity of the bond’s price to changes in the share price) increases and the arb traders short more MicroStrategy shares. When the MicroStrategy share price then decreases, the bond’s delta decreases and the arb traders buy back a portion of their shorts at a profit.

- Step 4b. If the MicroStrategy share price decreases, the bond’s delta decreases and the arb traders buy back a portion of their shorts at a profit. If the MicroStrategy share price then increases, repeat step 4a.

It’s important to note that this strategy relies on price volatility. Convert arb traders profit from price fluctuations — both up and down — and therefore cannot succeed if the price only trends upward.

BOND MARKET DESPARATE FOR YIELD

The bond market is desperate for positive yield due to persistently low interest rates and inflation eroding real returns, leaving investors with limited options. MicroStrategy is an escape route.

One category of investors buys the bonds for Bitcoin upside without downside risk. Another category of investors engages in convertible bond arbitrage, profiting from risk-free premiums by shorting the stock.

Convertible bonds become more attractive when MicroStrategy’s stock price falls because the bond itself becomes cheaper because its value depends partly on the stock price. When MicroStrategy’s stock price decreases, the conversion option becomes less valuable, decreasing the bond’s price. When MicroStrategy’s stock price increases, the conversion option becomes more valuable, increasing the bond’s price.

MicroStrategy is the ultimate Bitcoin buffet that feeds every investor taste and appetite.

“…converts can be issued at a premium to share price when shares are trading at 1x mNAV. Higher multiples are a downstream effect, not a primary cause, of the anticipation of further bitcoin purchases.” — @btc_overflow

ZERO COUPON & NEGATIVE COUPON CONVERTIBLE BONDS

MicroStrategy has the potential to leverage both zero coupon and negative coupon bonds.

A zero coupon bond pays no interest but is issued at a discount, repaying full value at maturity.

A negative coupon bond requires the investor to pay interest, effectively reducing the bond’s repayment amount.

Both zero coupon and negative coupon bonds appeal to investors who prioritise potential stock gains through conversion, rather than earning regular interest payments.

ONLY MICROSTRATEGY CAN OFFER BITCOIN BACKED BONDS

MicroStrategy is uniquely positioned as the only company able to issue sizeable bonds backed by Bitcoin.

With MicroStrategy’s substantial Bitcoin holdings on its balance sheet, it can offer significant collateral to support debt offerings.

At present, no other company comes close to matching MicroStrategy’s reserves, making it a monopoly in this regard.

“We’re the only company that can actually create bonds backed by Bitcoin. That’s the big idea.” — Michael Saylor

CONVERTIBLE BONDS & INSURANCE COMPANIES

Insurance companies that buy Bitcoin directly face write-downs which decrease reserve ratios.

Insurance companies that buy Bitcoin indirectly through MicroStrategy convertible bonds face no write-downs which maintains reserve ratios whilst still benefitting from Bitcoin’s potential upside.

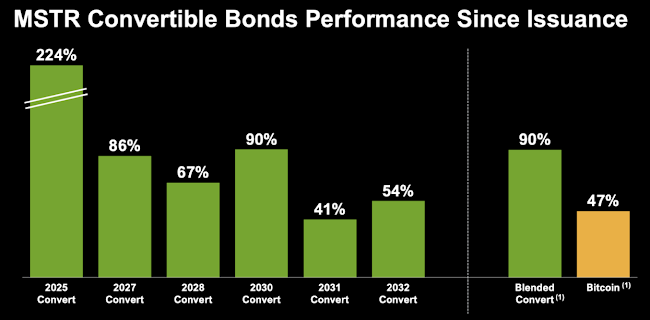

MICROSTRATEGY PERFORMANCE OF CONVERTIBLE BONDS SINCE ISSUANCE

5 out of the 6 convertible bonds issued by MicroStrategy to date have outperformed Bitcoin itself.

“MSTR’s Bitcoin derivative products have been met with unimaginable demand — breaking historical records and topping a range of financial metrics such as performance, options open interest, volume relative to market cap and volatility.” — @BitStrategy21

LOW LEVERAGE RATIO

MicroStrategy attempts to maintain a leverage ratio of ~25% — similar to a homeowner who only finances 25% of a house’s value — which is considered low-risk.

Each time a convertible note is converted and their leverage falls below their 25% target, they are prompted to enter the capital markets again.

MicroStrategy’s model is highly flexible, giving them options to adjust for market conditions while maximising shareholder value and Bitcoin exposure without excessive risk.

“We try to evaluate all options, we keep our options open, and we ask ourselves the question, is this prudent? And then also, is this accretive? Is this going to be good for our shareholders? And of course, with any discussion of leverage, we don't want too much. We want to just pick just the right amount of leverage, the leverage that allows us to benefit our shareholders without creating undue uncertainty. Sometimes it's appropriate to go fast. Sometimes it's appropriate to go slow. Sometimes it's appropriate to do nothing and wait for better opportunities to present themselves. The nice thing about our situation right now is that, we have all these options and we believe we're structured very, very well to take advantage of opportunities as they present themselves in the bitcoin era of institutional adoption that we see over the coming 15 years.” — Michael Saylor, Q1 2024 Earnings call

PREFERRED STOCK

Preferred stock is a hybrid financial instrument that combines features of both debt and equity, offering fixed dividend payments with no maturity date.

It ranks above common stock but below debt on a company's capital structure. This means that preferred stock shareholders are paid dividends before common shareholders but after debt holders.

Preferred stock doesn’t dilute or impact voting rights because it typically lacks voting privileges, leaving common stockholders’ control unaffected.

AT-THE-MARKET OFFERINGS (ATM)

ATM usage strengthens the balance sheet, by increasing equity, which increases borrowing capacity (leverage on the balance sheet) and allows MicroStrategy to switch from ATM to convertibles.

LARGEST CORPORATE HOLDER OF BITCOIN

MicroStrategy currently holds more Bitcoin than any other publicly traded company and significantly more than the next largest holder, putting it in a position to achieve a monopoly.

“The key idea is that one company can be the leading Bitcoin Bank. To be that company, you need to be 150% bitcoin.” — Michael Saylor

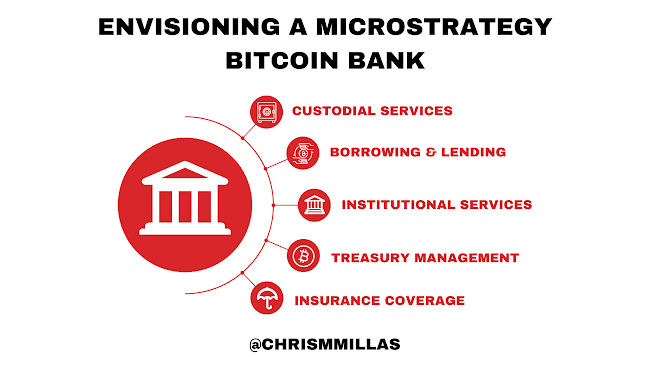

BECOMING A GLOBAL BITCOIN BANK

MicroStrategy is poised to become the biggest global Bitcoin Bank.

As the largest corporate holder of Bitcoin, MicroStrategy can leverage its holdings by offering financial products and services backed by Bitcoin.

As a Bitcoin Bank, we could estimate MicroStrategy to generate cash flows based on an annual yield of ~4% relative to the total value of its Bitcoin holdings. Thus, the more Bitcoin MicroStrategy holds and the higher the price of Bitcoin, the more cash flows it will generate.

“Actually there is a very good reason for Bitcoin-backed banks to exist, issuing their own digital cash currency, redeemable for bitcoins. Bitcoin itself cannot scale to have every single financial transaction in the world be broadcast to everyone and included in the block chain.” — Hal Finney

"We live in a world right now where it's difficult to live off of your accumulated capital without actually being in the business of taking risk. I guess that's what I'm getting at. I think Bitcoin offers a different possibility. I see a world — we're not there yet — but I think 10 years out, I see a world where you would be able to take your Bitcoin, put it with a trustworthy bank and the bank would lend it out. They would give you a yield, and you could then never sell your Bitcoin, pay your living expenses with the yield the bank gave you and then the Bitcoin would appreciate in fiat terms forever." — Michael Saylor

POISED TO DOMINATE THE FIXED INCOME MARKET

Michael Saylor has explicitly stated that he wants MicroStrategy to become the “Amazon of fixed income,” implying he wants the company to become the go-to platform for bond investors by leveraging its Bitcoin holdings.

For context, the fixed income market is currently worth ~$100T.

Therefore, even if MicroStrategy’s software business ceased to operate, the company can continue to grow based solely on its capital markets activities, using its Bitcoin holdings as collateral.

“We want to be the Amazon of fixed income.” — Michael Saylor

INDEXES INCLUSION

The more indexes that MicroStrategy is added to, the more passive flows it attracts, forcing indexes to purchase shares regardless of the price.

The more passive flows MicroStrategy attracts, the higher its share price, the more capital it can raise, the more bitcoin it can buy, the more the price of Bitcoin increases, the bigger its market cap, the bigger the weighting in indexes, the more passive flows it attracts, creating a flywheel effect.

“I don’t think [@saylor] is speculative attacking the dollar…he’s speculative attacking the U.S. stock market & passive income flows…he’s about to make it into the S&P 500 where he can perform the vampire attack of all vampire attacks...” — @americanhodl8

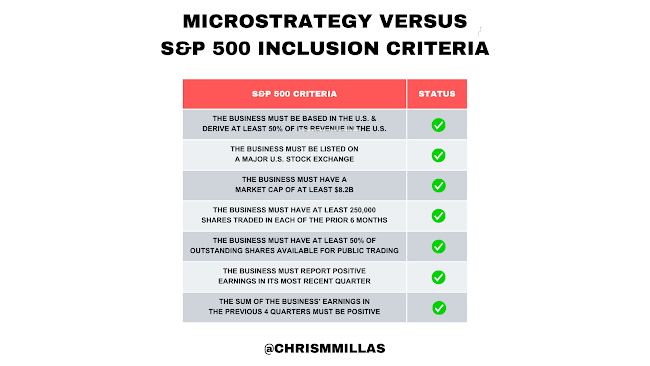

MICROSTRATEGY VERSUS S&P 500 INCLUSION CRITERIA

ADOPTION OF NEW FASB RULES

Before the Financial Accounting Standards Board (FASB) rule changes, MicroStrategy had to report its bitcoin holdings at their lowest value each quarter, reflecting any decreases in value but not increases.

After the Financial Accounting Standards Board (FASB) rule changes, MicroStrategy can report its bitcoin holdings at their fair value (the value of its holdings at the time of each quarter’s reporting).

This will positively impact MicroStrategy’s Net Asset Value (NAV) and NAV multiple, driving its stock price up.

BEAR MARKET PROTECTION? (UNLIKELY)

Some people believe MicroStrategy can protect itself/Bitcoin from a bear market.

This is overly-optimistic in my opinion. While I understand the reasoning, at a basic level it ignores two things; investor psychology and global liquidity.

Firstly, fear and greed will always drive irrational behaviour that leads to over-corrections in both bull and bear markets. It’s human nature. If you needed reminding, MicroStrategy traded below its NAV during the 2022 bear market. It’s easy to forget what things are like when sentiment is at its lowest.

For the record, 30-40% of MicroStrategy shares are owned by retail investors — those who are most vulnerable to emotional decision-making and panic selling.

Secondly, global liquidity drives asset prices. For context, global liquidity has a ~97% correlation with the $NDX and a ~85% correlation with $BTC.

$BTC is also one of, if not, the most liquid asset, hence why it is so sensitive to moves in global liquidity. Historically, for every ~10% move in global liquidity, Bitcoin has moved by ~45%.

Thus, a fall in global liquidity during a bear market will mean a relative fall in the price of both $BTC and $MSTR.

So, while MicroStrategy may dampen a bear market to some degree, expecting it to prevent one entirely is misguided in my opinion — unless, of course, we get hyperbitcoinisation.

THE RISKS

MAIN RISKS

- Bitcoin Extinction

If Bitcoin suffers an existential collapse — due to a critical security flaw, a Black Swan event or something else — MicroStrategy fails since its value is directly tied to Bitcoin’s success.

MicroStrategy will live or die based on Bitcoin.” — Saylor

- Prolonged Decline In Bitcoin Price

If Bitcoin suffers a prolonged and significant decline in price due to, for example, a severe financial crisis, it could force MicroStrategy to significantly dilute its shares in order to repay a convertible bond that is due to mature.

While the risk is low, it remains one of the biggest threats.

OTHER RISKS

- Maintaining Volatility (Low Probability)

Volatility risk lies in the fact that MicroStrategy’s stock must remain volatile enough to attract convertible bond buyers whilst ensuring that there is sufficient demand from these buyers to issue bonds at scale.

- Operational Risk (Low Probability)

MicroStrategy’s operational risk includes the potential loss of its Bitcoin due to security breaches, custodial failures or regulatory seizure.

- Low Or No Demand For A Bitcoin Bank (Low Probability)

Low or no demand for a Bitcoin Bank that provides financial instruments, such as loans, backed by Bitcoin would prevent MicroStrategy from leveraging its Bitcoin holdings to generate cash flows.

- Regulatory (Low Probability)

Regulatory risk lies in changing laws around Bitcoin that could adversely impact the Bitcoin industry more generally and MicroStrategy specifically.

- Counterparty Risk (Low Probability)

Counterparty risk lies in MicroStrategy’s reliance on debt financing and external capital markets to sustain its Bitcoin strategy. If lenders or markets lose confidence or restrict access to capital, MicroStrategy may struggle to continue growing its Bitcoin holdings.

- Executive Order 6102 (Low Probability)

Executive Order 6102 risk lies in the possibility that the government could enact a policy similar to Executive Order 6102 which banned gold hoarding during the Great Depression as a result of the financial crisis. This would enable government to either restrict or seize MicroStrategy's Bitcoin holdings.

While the probability of this being enforced is low, it will always remain a risk.

- Key-Man Risk (Low Probability)

Key-man risk lies in the potential loss of leadership of Michael Saylor.

This risk is overstated in my opinion for 3 main reasons.

- The beauty of the Bitcoin strategy is that — paradoxically — it’s so simple that almost anyone can execute it.

- Most of the heavy lifting has already been done. MicroStrategy has, for all intents and purposes, secured monopoly status.

- Whoever replaces Saylor would be well aware that any deviations from the playbook he has laid out would not go down well with shareholders. They’d be incentivised to follow Saylor’s lead to a T.

Let me make it clear; I would prefer to have Saylor at the helm than not — obviously — but I do not see his absence as a major risk to the long-term thesis.

In the words of Buffett: “I try to invest in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.”

- No Capital Gains Tax On Bitcoin

If Bitcoin becomes exempt from capital gains tax, investors may prefer holding Bitcoin directly, thus reducing the appeal of MicroStrategy as an alternative Bitcoin investment vehicle.

While this is a risk, the reality is that the added value that MicroStrategy provides is likely to offset any savings in capital gains from buying Bitcoin directly.

THE MANAGEMENT

The most effective leaders and organisations have range; they are paradoxical. They are demanding and nurturing, orderly and entrepreneurial, hierarchical and individualistic all at once.

“I learned to go into business only with people whom I like, trust and admire.” ― Warren Buffett

“Good jockeys will do well on good horses, but not on broken-down nags. When a management team with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the company that remains intact.” — Charlie Munger

MAIN EMPLOYEES

MICHAEL SAYLOR

Michael Saylor co-founded MicroStrategy in 1989.

In the 1990s, MicroStrategy experienced rapid growth, with its innovative approach to business intelligence software. The company went public in 1998, benefiting from the dot-com boom. Its stock soared and Saylor became known for his ambitious vision for the digital future.

However, the early 2000s brought significant challenges. In 2000, the company faced a financial restatement crisis that led to a sharp decline in its stock price and legal troubles. This period marked a significant setback for MicroStrategy and Saylor, but it was also a turning point. The company refocused its business strategy, which eventually stabilised its operations and finances.

Over the next two decades, Saylor steered MicroStrategy through the evolving landscape of technology, with a focus on business intelligence, mobile software and cloud services. The company made significant investments in R&D and acquisitions to bolster its product offerings and market position.

Throughout his time at the company, Saylor has been a prominent and sometimes polarising figure. He is known for his visionary ideas about technology and the digital economy, as well as his bold business decisions. His leadership has taken MicroStrategy through periods of innovation and growth, as well as times of controversy and challenge, reflecting the dynamic nature of the tech industry.

Many will argue that Saylor has an unmatched understanding of Bitcoin.

Outside of MicroStrategy and Bitcoin, Saylor in an intense guy. One note-worthy story includes taking a date to the office, handing her a book and asking her to read all day while he worked while another story involved Saylor flipping his red Toyota sports car several times on an icy highway, escaping with cuts and bruises and heading back to his job. For fun, Saylor reads two-inch-thick tomes on the history of Western civilization after he gets home from work…at midnight.

Since 2014, Saylor has received an annual salary of $1. His total compensation in 2023 was reported as $799,670, with the majority stemming from other forms of compensation rather than base salary.

Saylor is a genuine rare breed. He is a man of the people.

Michael Saylor was the longest reigning CEO of a publicly traded software company, even managing to survive a devastating -99.8% stock price crash in MicroStrategy from $333 to $0.42 during the early 2000’s dot-com crash.

GENERAL

IS THE BUSINESS FOUNDER-LED?

Founder-led businesses tend to outperform (7%).

- Yes

“The company is going to rise and fall with the CEO.” — Carl Icahn

DOES MICHAEL SAYLOR GENUINELY POSSESS ANY OF THE “BIG 5” COMMON TRAITS ASSOCIATED WITH INNOVATORS?

- Openness to new ideas.

- High conscientiousness (willingness to apply themselves over many years).

- High disagreeableness (not easily dissuaded).

- High IQ (ability to synthesize information quickly).

- Low neuroticism (ability to handle stress).

We can make an extremely convincing case that Michael Saylor possesses all 5.

IS MICHAEL SAYLOR DRIVEN BY INTERNAL (GOOD) OR EXTERNAL (BAD) REWARDS?

- Internal

DOES MANAGEMENT THINK LONG-TERM?

- Radically

DOES MANAGEMENT HAVE MEANINGFUL SKIN IN THE GAME?

Yes. Michael Saylor owns approximately 13.9% of MicroStrategy's outstanding shares.

DOES MANAGEMENT ACT IN THE BEST INTERESTS OF ITS SHAREHOLDERS?

- Radically

"If you own MicroStrategy you’re my partner. You and I are in it together." — Michael Saylor

IS MANAGEMENT DETAIL ORIENTED?

- Radically

IS MANAGEMENT INNOVATIVE?

- Radically

IS MANAGEMENT MISSION DRIVEN?

A leader must be a true believer in the mission.

- Radically

IS MANAGEMENT RATIONAL?

- Radically

IS MANAGEMENT CANDID WITH SHAREHOLDERS?

- Radically

HAS MANAGEMENT DEMONSTRATED LEADERSHIP QUALITIES?

Leadership is the single greatest factor in any team’s performance. There are no bad teams, only bad leaders.

- Yes

HAS MANAGEMENT DEMONSTRATED A HIGH DEGREE OF INTEGRITY?

- Yes

HAS MANAGEMENT DEMONSTRATED A HIGH DEGREE OF INTELLIGENCE?

- Yes

HAS MANAGEMENT DEMONSTRATED A HIGH DEGREE OF ENERGY?

- Yes

DOES MANAGEMENT RESIST THE INSTITUTIONAL IMPERATIVE?

- Yes

ARE INCENTIVE PROGRAMS ALIGNED WITH SHAREHOLDERS?

- Yes

DOES MANAGEMENT HAVE A TENDENCY TO UNDER-PROMISE & OVER-DELIVER OR OVER-PROMISE & UNDER-DELIVER?

- Under-promise & Over-deliver

CULTURE

DOES THE BUSINESS HAVE A STRONG CULTURE?

Companies with strong cultures tend to outperform. Strong cultures tend use the word "family" to describe their relationship with others.

Yes. In an extract from an article written in 2,000, the author writes the following:

“Saylor takes his employees’ happiness extremely seriously. To him, MicroStrategy is less a company than a nation of which he is President, and if someone quits he feels it personally, like a lost vote. He keeps track of how many people have left since the company started, and he wonders why they left. Each year, he pays for a Caribbean cruise for his entire staff, to build company solidarity.”

CAN THE BUSINESS ATTRACT & MAINTAIN TALENT?

MicroStrategy can attract the best talent because of the potential financial upside individuals can benefit from by having equity (options) in the business.

THE FINANCIALS

STOCK BASED COMPENSATION

WHAT IS THE BUSINESS’ STOCK BASED COMPENSATION PHILOSOPHY?

- TBC

IS STOCK BASED COMPENSATION LINKED TO MANAGEMENT PERFORMANCE OR STOCK PRICE?

- TBC

IS STOCK BASED COMPENSATION < 15% OF REVENUE?

- Yes

IS THERE NO PREFERRED STOCK ON THE BALANCE SHEET (BUFFET RULE)?

- Yes

“A stock option is both an expense and dilution. To argue anything else is insane.” — Charlie Munger

THE MARKET

VALUATION

All models are wrong. Some are useful.

At a basic level, this is how I think about and frame MicroStrategy’s market cap:

MicroStrategy’s market cap is a reflection of the real-time value (RTV) of the total number of Bitcoin the market anticipates the company to acquire over time combined with the present value (PV) of all future Bitcoin-related profits that the market anticipates the company to generate over time.

So as a formula:

$MSTR Market Cap = RTV Total Bitcoin Acquisitions + PV Future Bitcoin-Related Profits

I then apply two premiums:

- A 50% premium for MicroStrategy being a monopoly.

- A 15% premium for Michael Saylor.

It’s important to note that MicroStrategy should be evaluated and valued in both fiat and Bitcoin terms and considered separately.

Only infinite fiat generates a large premium. On a Bitcoin standard, monetary debasement is eliminated, leading to stable purchasing power and a deflationary environment. This reduces the speculative need to pay high premiums for assets.

You can access my latest model and plug in your own numbers on X (Twitter) here.

Note: Both future Bitcoin Yield and future cash flows generated from Bitcoin holdings deserve a multiple. Future Bitcoin price appreciation does not.

MicroStrategy has no ceiling because the Dollar has no floor.

Over a long enough time horizon, MicroStrategy will go from $100B to $1T to $5T to $10T to $15T to $20T.

“If you think about what they can do with their Bitcoin stash in the future, that’s easily justifiable up to the 20-30x mNAV.” — Samson Mow

HOW MICROSTRATEGY BENEFITS FROM A HIGH NAV MULTIPLE

The higher MicroStrategy's NAV premium, the more accretive their Bitcoin yield strategy becomes, since they can buy more Bitcoin by selling less shares, thus decreasing dilution and increasing Bitcoin Per Share.

“So, what's the right multiple to put on a company that generates dividend yield? It could be 10x, it could be 20x, it could be 30x. It comes down to - do you think the yield will continue? And is there a growth rate? MicroStrategy generated close to 18% Bitcoin yield this year.” — Michael Saylor

HOW WIDE IS THE RANGE OF EXPECTED VALUES?

- Low

- Medium

- High

“Underpriced is far from synonymous with going up soon…Being too far ahead of your time is indistinguishable from being wrong…It can require patience and fortitude to hold positions long enough to be proved right.” — Howard Marks

“What the wise man does in the beginning, the fool does in the end.” — Warren Buffett

“Being very early and being wrong look exactly the same 99% of the time.” — Seth Klarman

DOES THE BUSINESS BUYBACK SHARES?

Companies that repurchase shares tend to outperform the market.

Historically yes, although this has been less relevant since MicroStrategy adopted its Bitcoin strategy.

"Buying back shares is the simplest and best way a company can reward its investors. If a company has faith in its own future, then why shouldn't it invest in itself, just as the shareholders do?" — Peter Lynch

IS THE RISK ASYMMETRICAL?

- Yes

"[MicroStrategy] still has a massive runway ahead of it [at ~$100). It's our position that we are in the very early innings today of a massive capital repricing event." — Bill Miller IV

“Warren is scanning the world trying to get his opportunity cost as high as he can so that his individual decisions are better.” — Charlie Munger

“Everything is a function of opportunity cost.” — Warren Buffett

“Outperforming the market with low volatility on a consistent basis is an impossibility. I outperformed the market for 30-odd years, but not with low volatility.” — George Soros

OTHER

IS THE THESIS SIMPLE OR COMPLEX?

The MicroStrategy thesis can be distilled down to 2 simple ideas:

- In the short-term, leverage debt to maximise Bitcoin holdings.

- In the long-term, leverage Bitcoin holdings to maximise cash flows.

Everything else is details.

Once you truly see what MicroStrategy is doing, you can’t unsee it.

"One of the greatest ways to avoid trouble is to keep it simple." — Charlie Munger

IS THE THESIS EXPANDING OR CONTRACTING?

- Expanding.

“A good thesis is one that holds over time. A great thesis is one that expands over time.” — @ryQuant $MSTR

WHAT IS THE PROBABILITY OF PERMANENT CAPITAL LOSS?

- <2%

THE PERSONAL

ON A SCALE OF 1 TO 10, HOW WELL DO YOU UNDERSTAND THE BUSINESS?

- 9

"Extreme patience combined with extreme decisiveness. You may call that our investment process. Yes, it's that simple." — Charlie Munger

ON A SCALE OF 1 TO 10, HOW WELL DO YOU UNDERSTAND THE THESIS?

- 9

"A lot of great fortunes in the world have been made by owning a single wonderful business. If you understand the business and you know what you are doing, you don't need very many of them." — Warren Buffett

DO YOU HAVE AN EDGE IN UNDERSTANDING THIS BUSINESS? IF SO, WHAT IS IT?

To make money, you need to make a contrarian bet that eventually becomes convention.

Yes. The market has yet to wake up to how Bitcoin is transforming money and how MicroStrategy is transforming financial markets.

“What you have to learn is to fold early when the odds are against you or if you have a big edge, back it heavily because you don't get a big edge often. Opportunity comes, but it doesn't come often, so seize it when it does come.” — Charlie Munger

DOES THIS INVESTMENT ALIGN WITH YOUR PERSONALITY & INVESTING PHILOSOPHY?

- Yes

“Part of the game of investing is to 'come into your own.' You must find some way that perfectly fits your personality.” — Li Lu

ON A SCALE OF 1-10, HOW MUCH DOES YOUR INTUITION RESONATE WITH THIS INVESTMENT?

- 9

“Very few companies make it through our filtering system as potential investment and even fewer make it into our portfolio.” — Terry Smith

ARE YOU THINKING INDEPENDENTLY & NOT BEING INFLUENCED BY GROUPTHINK?

- Yes

“Part of what you must learn is how to handle mistakes and new facts that change the odds. Life, in part, is like a poker game, wherein you have to learn to quit sometimes when holding a much–loved hand.” — Charlie Munger

ARE YOU EVALUATING THINGS OBJECTIVELY & NOT FALLING PREY TO CONFIRMATION BIAS?

- Yes

“Look, my job is essentially just corralling more and more and more facts and information, and occasionally seeing whether that leads to some action. We don’t read other people’s opinions. We want to get the facts and then think.” ― Warren Buffett

IS THIS A "MUST-OWN” OR “NICE-TO-OWN" INVESTMENT?

The more concentrated your portfolio, the higher your chances of beating the market. Note that you will also endure longer periods of underperformance. e.g. Keynes and Munger underperformed 1/3 of the time.

Since excellent companies are rare, not buying should be the default.

You must attempt to make less bad investments than more good investments.

Buy the best. Ignore the rest.

Bet big on a winner because the less you bet, the more you lose when you win.

- Must-Own

"We are massive bulls on MicroStrategy. It's our largest position." — Bill Miller IV

"Opportunity doesn't come often — so seize it when it comes." — Charlie Munger

“A few good ideas is all you need. And when you find the few you have to act aggressively.” — Charlie Munger

“The one thing all those winning bettors in the whole history of people who've beaten the parimutuel system have is quite simple: they bet very seldom.” — Charlie Munger

“The way to get rich is to put all your eggs in one basket and then watch that basket” — Andrew Carnegie

IS IT A GREAT COMPANY — ONE THAT WILL BE AROUND IN 25 YEARS?

The longer the time period, the stronger the correlation between price and intrinsic value.

Yes. The Lindy Effect would also suggest so since MicroStrategy has been around since 1989.

“The definition of a great company is one that will be great for 25 or 30 years.” — Warren Buffett

WOULD YOU BE COMFORTABLE HOLDING ONTO THIS INVESTMENT FOR 10 YEARS?

- Yes

"Only buy something that you'd be perfectly happy to hold if the market shut down for 10 years." –– Warren Buffett

IS THIS BUSINESS WITHIN YOUR CIRCLE OF COMPETENCE?

- Yes

"We know the edge of our competency better than most—that's a very worthwhile thing. It's not a competency if you don't know the edge of it." — Charlie Munger

“Investors who invest outside their circle of competence can find themselves in big trouble.” — Charlie Munger

FREQUENTLY AMPLIFIED QUALMS (FAQ)

All $MSTR bear arguments can be dismissed with the same single 5-word response: “Saylor is the largest shareholder.”

- Q) “MicroStrategy is a Ponzi.”

MicroStrategy is a leveraged Bitcoin holding company. The same way real estate investors leverage debt to increase their real estate holdings, MicroStrategy leverages debt to increase its Bitcoin holdings.

“I would call it an economy.” — Michael Saylor

- Q) “MicroStrategy is a scam.”

A) MicroStrategy captures low frequency analogue energy — fiat — that is decreasing in value and transmutes it into high frequency digital energy — bitcoin — that is increasing in value. In doing so, it is accelerating the global transition to a Bitcoin standard.

- Q) “MicroStrategy is a closed-end fund. You might as well just buy a Bitcoin ETF.”

Through its ability to intelligently leverage capital markets and accretive dilution, MicroStrategy offers investors amplified exposure to Bitcoin for every unit of currency invested by actively increasing its Bitcoin Per Share (BPS). MicroStrategy offers other additional benefits too compared to an ETF — see “MicroStrategy Versus Other Bitcoin Investment Vehicles” chart.

“Owning MicroStrategy is better than owning a Bitcoin ETF.” — @billfour

- Q) “You should just buy Bitcoin.”

A) There are no rules. Everyone is optimising for different goals. People who are optimising for self sovereignty buy Bitcoin. People who are optimising for ROI buy MicroStrategy. Or a mix of both. Both assets come with pros and cons. Everything is trade-offs — see “MicroStrategy Versus Other Bitcoin Investment Vehicles” chart.

- Q) “The software business is trash.”

A) MicroStrategy is not dependent on the success of its software business to pursue its Bitcoin strategy.

Thus, MicroStrategy’s borrowing capacity is not constrained by the earnings capacity of its software business.

There are no bond covenants requiring interest payments to come from operating cash flows. MicroStrategy can finance its interest costs — through either debt or equity — without selling a single Bitcoin.

- Q) “Saylor has been selling shares.”

A) Saylor sold shares between February 1, 2024 and April 26, 2024, which were granted to him in 2014 as part of his compensation package. Had he not exercised these options, they would have expired worthless. Since 2014, at his own request, Saylor has been on a $1 salary and has opted not to receive any cash bonuses.

- Q) “MicroStrategy will get liquidated.”

A) MicroStrategy’s debt is not structured like a traditional margin loan, where assets risk liquidation if the collateral value drops below a certain threshold.

Instead, MicroStrategy uses fixed-rate, low or zero-interest, long-term, unsecured convertible debt, giving it ample time and flexibility to manage its obligations and navigate inevitable market fluctuations.

In an extreme scenario where Bitcoin drops dramatically for a prolonged period and MicroStrategy is forced to repay a convertible bond because it hasn’t hit its conversion price, the debt would be equitized. While dilutive to existing shareholders, this outcome avoids default and liquidation of Bitcoin holdings.

RECOURSES

ANALYSTS

High T MSTR: https://x.com/i/communities/1873795169054597544

QuantBros: @PunterJeff | @RyQuant| http://youtube.com/@Quant_Bros/

General: @Adrian_R_Morris | @Z06Z07 | @DylanLeClair_ | @btcjvs | @dgt10011 | @BitStrategy21 | @TheJesseMK |

MSTR Convertible Notes: @BenWerkman | @RichardByworth

MSTR Options: @hillery_dan | @nithusezni | @ActuallyClimber

MSTR True North: @MSTRTrueNorth

MSTR Interviews: @TimKotzman | http://youtube.com/@timkotzman8925

MSTR Art: @LaDoger21

IL MSTR: @masonfoard | https://x.com/i/communities/1761182781692850326

MSTR On Discord: @80IQmindset | http://discord.gg/mstrden

MSTR Daily: @matt_utxo | http://youtube.com/@MSTRDaily

MicroStrategy Today: @MMMicroStrategy | https://youtube.com/@microstrategytoday

MSTR Tracker: @LizardWizardBTC | @MSTR_Tracker | http://mstr-tracker.com

Saylor Tracker: http://saylortracker.com

MSTR Portfolio Explorer: http://microstrategist.com

MSTR Catalyst & Convertible Debt Tracker: @Max_Colbert | http://mstrmoon.com

Bitcoin Treasury Tracker: http://treasuries.bitbo.io

Saylor Interviews: https://spoti.fi/3BkApxD

H/T

@ryQuant, @PunterJeff, @billfour, @adam3us, @hillery_dan, @Z06Z07, @Adrian_R_Morris, @BenWerkman, @BitStrategy21, @80IQmindset, @btcjvs, @BritishHodl, @TomerStrolight, @PrestonPysh, @btc_overflow and others.

ARTICLES

- https://www.washingtonpost.com/archive/business/1996/07/15/from-the-ground-up-and-up/09c40522-b92a-4349-9895-73352973b6c0/

- https://www.newyorker.com/magazine/2000/04/03/caesar-com#:~:text=Saylor%20takes%20his%20employees'%20happiness,personally%2C%20like%20a%20lost%20vote

SORT

- A MicroStrategy stable coin could generate additional income.