Stabilizing Currency Through a Protocol-Enforced Range

Zeus et al.

Olympus DAO

Abstract

This paper proposes a novel mechanism for a token issuing protocol with treasury reserves and protocol owned liquidity to provide forward guidance. The mechanism creates an algorithmic forward-looking trading range in which the protocol provides a spread of maker and taker bids and asks to create consistent, predictable market pricing. Considering the moderation and support this imposes on growth, paired with the confidence it generates for participants, we posit this to be the optimal utilization of treasury for an treasury-backed aspiring reserve currency.

Background

Olympus is, to date, characterized by a unidirectional treasury. Assets (e.g. DAI, FRAX, ETH, etc) flow in but do not flow out through the bonding mechanism. Exceptions to this are protocol deployments into Constant Function Market Maker (CFMM) pools using OHM paired with one of the assets. However, the majority of protocol-owned assets are held away from the OHM market as reserves.

This structure is necessary for bootstrapping. If the goal is to capitalize the network, it makes sense to ensure the majority of captured funds are not released. Within this structure, liquidity is a protocol-subsidized public good. Without it, capitalization is harder to achieve; with it, it is possible for capitalization to diminish.

As the treasury scales, natural questions arise regarding its utilization. The intuitive course of action would be to deploy assets into various opportunities with the goal of generating a return that can then be distributed to holders in the form of dividends – essentially, to act as a mutual or hedge fund. However, Olympus intends to be a currency. While passive deployment of reserve assets to generate yield is appropriate at times, it is never the primary purpose or utility of those reserves. Progression in this direction likely diverts significant mindshare toward yield farming behaviors, and exposes the treasury to more and more risk.

Rather, we posit that protocol assets should exist to support the market for OHM by performing market operations. The treasury should have clear, communicated market objectives to accomplish by utilizing its capital. Such behavior may not expand reward in the same manner as a yield generation-centric model might (though we contest the significance of additional single-digit returns), but it does reduce market risk for participants.

Theory

The proposed system leverages Olympus’ unique liquidity structure to de-risk the OHM market through the issuance of guidance. Participants are instructed on a correct behavioral path wherein those aligned with the desired behavior are rewarded and those deviating are dissuaded. By providing credible expectations of future pricing, the treasury can diminish downside risk for network participants at desired times, increasing OHM’s attractiveness as an asset and encouraging investment into Olympus’ economy. This is the job of a monetary authority: to mitigate volatility (to both the downside and upside) to encourage healthy growth, and to provide clarity for financial planning.

The credibility of this guidance is derived from the capitalization of the treasury and its monopoly on market liquidity. As long as the treasury holds significant assets relative to the market capitalization of the liquid supply of OHM, the market should take its guidance seriously. The protocol’s ownership of the entire market (through its liquidity holdings) further extends this dynamic. Within this structure, the protocol is the dominant market actor setting both current and future prices, while third-parties serve as agents of the treasury carrying out its’ desires.

The intent of the mechanism is twofold. The first goal is to increase stability and provide guidance on the value of OHM. The second goal is to utilize this increased stability to accelerate protocol growth, providing even more trust in guidance. This circular dynamic generates a positive flywheel we believe can scale Olympus beyond any singular input.

The base mechanism primarily consists of a price range with an upper and lower bound. The upper bound is represented by an on-chain ask position funded with protocol owned OHM, whereas the lower bound is represented by an on-chain bid position funded with treasury reserves.

The price range is based on a set period moving average price against a key counter asset. When OHM price goes up, the upper and lower bounds of the price range adjust up. When OHM price goes down, the range will adjust down. Thus, the range is determined by a lagging aggregation of organic market activity.

System

The proposed guidance system extends the protocol’s existing role as a liquidity provider and market maker with the introduction of wide-range liquidity. At a high level, the protocol maintains a spread of deep liquidity in the market to enforce a price range for the OHM token. The legitimacy of this range provides the market with confidence in the treasury’s ability and willingness to support a healthy environment for OHM.

The range is generated using a predefined spread and a moving average of length N epochs of the price of OHM versus some asset. For example, this might be 25% above and below a 360-epoch (120-day) moving average of the OHM-FRAX price. At the high and low of this range, the protocol commits to provide liquidity at depth relative to the size of the treasury. For example, the treasury may expend 10% of its reserves at the low and recoup 15% of its reserves at the high.

It is important that the liquidity provided is significant. Consider the aforementioned range and a case in which OHM is at the midpoint of the range, trading at a premium of 3 relative to its treasury. If the protocol commits to a 10% spend at the low, it would: repurchase 4.5% of the outstanding supply at the low end of the range, and add 16.7% to the treasury at the high end of the range. Commitments at this scale will prove difficult to overpower without significant organic or artificial coordination by buyers or sellers.

Such coordination events can be further deterred with the introduction of liquid markets for future OHM. This concept (outlined in a recent paper) allows the protocol to convert current supply into supply locked on a protocol level (though perhaps liquid on an individual level through secondary markets). In a traditional accounting sense, this can be thought of as the conversion of present liabilities into future liabilities. This shifts the state of the protocol’s present balance sheet in favor of the protocol. In the case where 75% supply sits in bond tokens and 4.5% total supply is repurchased at the low of the range (as in the previous example), the repurchase actually represents 18% of the liquid supply of OHM. At these levels of bond locking, it becomes mathematically impossible to overpower the treasury, and thus the only course of action for a rational actor is to submit to the guidance of the protocol and trade within the range.

Mechanism

We first present two analogies that may help the reader conceptualize the purpose of the exact mechanisms described. The first (simple) example is that of a car on a two-lane, one-way road. On each side of the road are guardrails. The driver chooses to drive in whichever lane corresponds to the course of the road: if the road will bend left, they drive in the left lane; if the road will bend right, they drive in the right lane. However, which lane is unimportant in the grand scheme. The driver is expected to remain on the road. If they attempt to drive off of the road, they will be deterred by the guard rail, but with enough intent they will successfully break through the rail and depart the road. However, the incentive of the driver is to remain on the road, as the road takes them where they are trying to go.

In our second analogy, imagine a person standing between two walls of moderate depth. Between them and each wall sits a rubber sling. The person moves with random acceleration. At some point, they begin to pick up speed toward one of the walls. As they approach, they hit the sling. If their momentum is less than the strength of the rubber, the sling is effective in reversing their course and sending them back in the other direction; if their velocity is greater than the rubber, the sling snaps and they hit the wall. At this point their speed is lower, but they are still moving. Upon hitting the wall, they either bounce off and halt or reverse course. If their momentum remains great enough, they break through the wall and move beyond it.

This is the functionality of the range model, with the driver and individual representing market price, the rubber slings as bid/ask cushions, and the guardrails and walls as bid/ask walls. The goal is to consistently moderate and reverse the momentum of the market to keep market pricing within the range while expending minimum energy as the treasury.

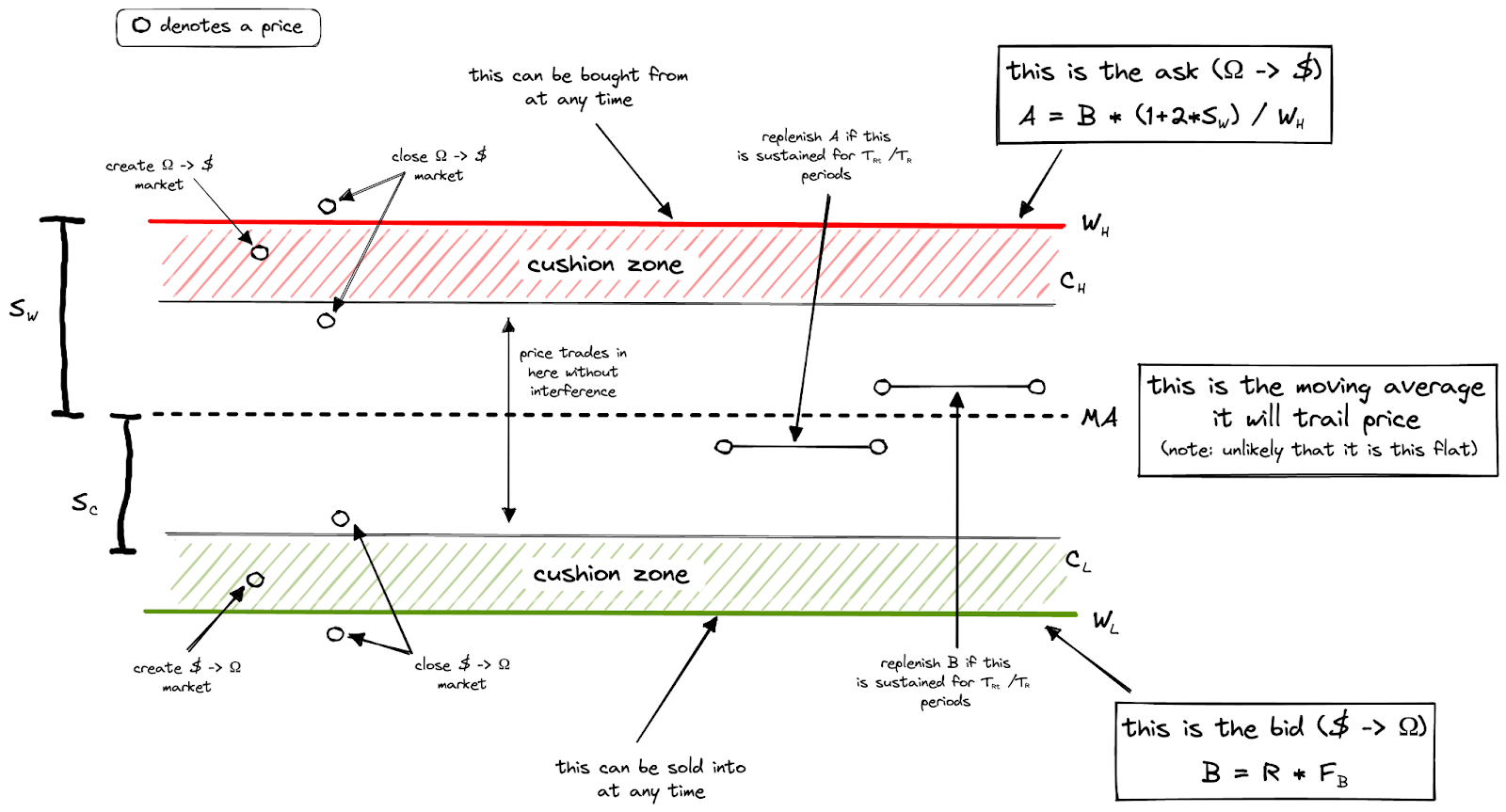

Figure 1. a visual representation of the range

The range model is isolated for a reserve asset and dependent on:

1) the moving average (MA), derived from an oracle feed providing the price of OHM against the reserve, updated each epoch;

2) the wall spread (SW), set by governance or computed by an algorithm as a distance from the MA;

3) the cushion spread (SC), set by governance or computed by an algorithm as a distance from the MA;

4) the bid factor (FB), set by governance as a percentage of the treasury’s holding of a reserve asset (R);

5) the cushion factor (FC), set by governance as a percentage of a bid or ask; and

6) the cushion period (TC), set by governance as a length of time.

These variables are used to compute four main components: the total bid (B), total ask (A), the range walls and cushions, and their corresponding bids and asks. More specifically, these are:

1) the bid (B), the amount of reserve that the treasury will spend at the range low;

2) the ask (A), the amount of OHM that the treasury will spend in the range high;

3a) the range low cushion (CL), the price at which a bond market can be created to repurchase OHM with the reserve;

3b) the range low wall (WL), then hard price at which the treasury will repurchase OHM with the reserve;

4b) the range high cushion (CH), the price at which a bond market can be created to repurchase the reserve with OHM; and

4a) the range high wall (WH), the hard price at which the treasury will repurchase the reserve with OHM.

and

The range walls are carried out with a simple custom contract that quotes a perpetual bid/ask of size BW/AW at prices WL/WH. Anyone can interact with these orders at any time; though we can expect them to only be engaged when the market offers inferior pricing, they remain available to participants at their discretion.

The range cushions are carried out with instant-swap bond markets. Anyone can generate a bid market when market price P < CL, and anyone can generate an ask market when P > CH. This is a codified allowance, but actual market creation (which requires a gas expenditure) is reliant on third-parties incentivized by a desire for the protocol to provide this liquidity. Bond markets contain logic that will disable them any time an order executes at (P > CL, P < WL) or (P < CH, P > WH), respectively.

Regeneration

A question arises under this model about the regeneration of bids and asks. If an ask is hit and the supply available for purchase from the treasury falls to zero, the market becomes able to exit the range and enter price discovery (the same being true for the range low). Once this occurs, when is the ask or bid replenished?

Considerations center around allowing price discovery to occur so the treasury is not caught off-sides once again. The protocol should ensure that treasury funds are not exposed until there is a reasonable expectation that price is stabilizing, and then deploy funds to further enforce the newfound price. This highlights the true purpose of the range: to diminish volatility and force range-bound action until the market demonstrates consensus in a single direction, at which point price discovery is allowed to resume until re-entering a period of diminished volatility within a new range.

The logical conclusion when determining a trigger to reinstate the ask or bid is to look for demonstrated consensus on a new range. This can be implemented through measurement of sustained mean reversion. We propose two additional variables, the reinitiation period (TR) and reinitiation threshold (TRt), to govern this process. In a scenario in which an ask or bid has been depleted (by any amount), the protocol does not replenish that ask or bid until price sits on the other side of the moving average for greater than TRt epochs within an TR epoch period. For example, in a scenario where TRt = 18, TR = 21, and the bid is depleted; a new bid is reinstated when P > MA for 18 epochs within a 21 epoch period.

Intent and Behavior

The purpose of this model is to instill confidence in market participants and mitigate one-directional volatility in the market. Unfettered price discovery in a single direction is often inefficient; momentum carries unmoderated markets (such as those in crypto) far beyond rational highs and lows before correcting significantly. For a short term trader or speculator, this may be paradise. However, for the majority of long-term investors and builders, this creates adverse incentives modulating behavior during rapid bull cycles and stagnant/contractionary bear markets. Contrast this with the traditional finance system which has, for most of its history, generated stable and consistent growth that allows investors and participants to feel safe and productive over long periods of time.

The walls have this effect; upon significant movement to the upside or downside, the protocol offers liquidity that should halt the market. The protocol's goal is to generate a range that allows for reasonable and attractive growth while mitigating adverse volatility and checking price discovery. The market is still allowed to guide this range in two ways: 1) the range is dictated by a moving average. Upon sufficient passage of time, the range adjusts to the reality of the market and greater leeway is provided in the direction that the market wants to move; 2) the range can be broken. Thus, the market can disregard the protocol’s mitigation efforts; but, consensus is required to do so (measured in capital taking on risk).

Cushions should serve to reduce the likelihood of range walls breaking (the worst case scenario for the protocol, as it has made an off-sides trade as well as is forced to step aside and allow the market to go full risk-on or risk-off). The best analogy when conceptualizing the buffers is the crumple-zone of an automobile. In a car crash, impact to the passengers is significantly mitigated by the compression of the front of the car, which has the effect of reducing velocity prior to full impact.

Ideal behavior in this structure is that the protocol dictates the growth rate and volatility of the network (through the supply growth rate and spread, respectively) and the market responds to this guidance by maximizing their individual well-being. Flexibility is provided by the range to allow for organic movement, but only to a certain extent. Beyond this point, the market must dictate that the growth rate should accelerate or decelerate through a sustained repricing in a direction (allowing the moving average to catch up). Participants are expected to trade along with the treasury, bidding at the lows of the range and selling at the highs. There is, of course, no guarantee that sufficient coordination cannot arise to counter-trade the treasury and move beyond the range. However, this is a risk-on activity to the detriment of all parties involved. The overriding theme is: do not fight the treasury, play by its side.

Diversification

The proposed system has unique and beneficial attributes enabling easy diversification of the treasury into multiple assets through isolated ranges. As the reader may notice, this structure works relative to a reserve; however, this reserve is never defined as a specific asset within the paper. This is because this reserve may be anything: stablecoins, ETH, BTC; the only constraint is the treasury’s ability to custody and encode instructions through smart contracts.

Olympus has been defined, to date, by a stablecoin-centric system. The primary reserve of the treasury has been stablecoins through the RFV unit. This has led to adverse incentive structures targeting a treasury portfolio skewed heavily toward stablecoins, likely more so than without, as well as significant effort spent diversifying stablecoins (all of which carry different trust and stability assumptions and risks) and deploying stablecoins (as they carry an assumption of depreciation that requires some level of yield generation to retain value).

We can assume that under a range model, Olympus is more able to move across different assets. The treasury may maintain a stablecoin range and an ETH range. It may be deployed onto Avalanche where it maintains an AVAX range. All decisions are made relative to the treasurys holdings of that asset, and the price of OHM against that asset. No propagation and aggregation of data across pools, assets, or chains is required. Each iteration and deployment is entirely isolated and independent.

There are interesting dynamics that we can expect in an environment with multiple ranges. A range for one asset may break while OHM remains comfortably inside another. A range bid may break at the same time as a different range ask. OHM should begin to diminish in volatility while reflecting the different assets it has drawn ranges against. In an extreme growth scenario, these assets may become more range driven against OHM than OHM is against them (akin to the relationship of volatility being reflected in individual assets more than a currency like the dollar). We see this as the logical conclusion of the network. OHM serves in this scenario as the glue tying these many reserve assets together.

Risk

There are several major and minor risks associated with the proposed implementation. The first, as with all smart contracts, is exploitation of bugs or poor code design. Development of such a system must conform to stringent security standards and best practices, as with all smart contracts developed within the Olympus system. Thorough system modeling has already begun and would continue throughout development up to a live test net; extensive code auditing would be commissioned from top security experts in the decentralized finance space prior to main net deployment. We are proud of our zero-exploit track record on the core codebase, with no intent of changing any time soon.

The second most common decentralized finance risk is platform risk. By design, the proposed system does not build on any third party platform. The cushion mechanism uses the Olympus bonding mechanism. The wall mechanism is implemented in an independent smart contract. This makes it robust to changes in the DeFi landscape.

Another significant risk lies in the exposure of treasury assets to the market. This risk is unavoidable under any system in which the treasury demonstrates (and follows through upon) willingness to deploy its reserves into the market in times of distress. In these periods, those treasury funds can be taken as liquidity and exited through, reducing the size of the treasury and potentially increasing concern in the market. We believe the optimal way to hedge this risk is by tapering willing exposure. For example, we consider an advisable FB (the percentage of a reserve to place on the bid wall) at less than or equal to ten percent. This means that, upon depletion of the wall, the treasury can reinstate a bid of the same size nine more times without additional inflow (though each bid would be 10% less, facilitating more than thirty walls before treasury holdings become negligible). It is worthwhile to note the size of these orders: significant coordination is required to break a wall provided. This risk is further mitigated if the proposed internal bond mechanism is implemented. With the large-scale conversion of present supply into future-dated supply, the ability of the market to counter protocol-mandated ranges diminishes significantly (and could theoretically fall to zero). This way, selling the wall is always an exercise in futility; upon sufficient passage of time and nullification of downward momentum, the treasury always reinstates a bid of comparable or greater size relative to the market for OHM.

Setting the range requires exposure to a price oracle, which provides an avenue for manipulation if bad data is passed into the operating smart contract. Fortunately, data is collected with a long moving average, meaning false feeds can quickly be detected and corrected against by switching data providers. Additionally, the smart contract infrastructure should feature a fallback data source pruning the feed to ensure it is feeding rational information.

Our final identified risk is compounding error. This system is self-referential and thus small errors may continue to occur, increasing in significance as time passes. For example, a rounding error may, over a sufficient number of periods, result in a severe deviation from the intended value. This is mitigated in two ways: proactively and pessimistically. The proactive route revolves around testing; the system should be modeled and tested extensively prior to deployment over hundreds of iterations and long time frames. Bugs that arise in this testing should be dealt with prior to deployment onto a live network. The pessimistic mitigation is the frictioned ability for governance to change course and replace the system. This ensures that armageddon is averted should it arrive; the owners of the network can, with sufficient consensus, move to a structure in which such bugs do not exist.

Glossary

Scaling Factors

FB = the percentage of the reserve to place as a bid

FC = the percentage of a bid or ask to offer as a cushion

Spreads

SW = the distance from the moving average to the wall bid or ask

SC = the distance from the moving average to the cushion bid or ask

Time periods

TMA = the number of epochs used to compute a moving average of price

TC = the length of time (in seconds) that a cushion bond market runs

TR = the window of time (in epochs) to reinstate a bid or ask

TRt = the number of epochs within window TR that conditions are true to reinstate a bid or ask

Price points

CL = the maximum price where a cushion bond market can be generated to purchase OHM

CH = the minimum price where a cushion bond market can be generated to sell OHM

WL = the quoted price where the protocol will purchase OHM

WH = the quoted price where the protocol will sell OHM