An overview of IFRS & Challenges involved in first time adoption The Institute of Chartered Accountants of India, Bangalore 1st December’2010

CA Aditya Singhal M.Com, FCA, DISA(ICAI)

Join IFRS professional group for regular IFRS update: http://finance.groups.yahoo.com/group/IFRS-Professional/

1

fin.

F1.

Authoritative literature

• IFRS

• IFRS

• IAS

• IFRIC

• SIC

• Order of authoritativeness

• IFRS including any appendices

• Interpretations

• Appendices to IFRS that do not form part of the standards

• Implementation guidance issued by IASB

2

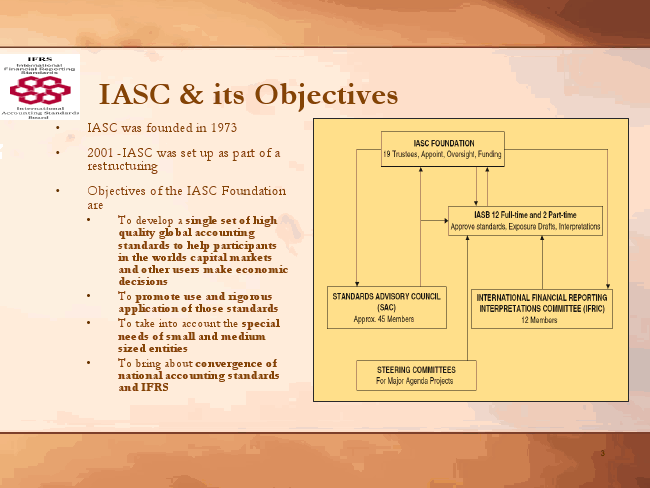

IASC & its Objectives

• IASC was founded in 1973

• 2001 -IASC was set up as part of a restructuring

• Objectives of the IASC Foundation are

• To develop a single set of high quality global accounting standards to help participants in the worlds capital markets and other users make economic decisions

• To promote use and rigorous application of those standards

• To take into account the special needs of small and medium sized entities

• To bring about convergence of national accounting standards and IFRS

3

in

IASC FOUNDATION 19 Trustees, Appoint, Oversight, Funding

i I X

IASB 12 Full-time and 2 Part-time Approve standards, Exposure Drafts. Interpretations

A

STANDARDS ADVISORY COUNCIL I I INTERNATIONAL FINANCIAL REPORTING

(SAO) | I INTERPRETATIONS COMMITTEE (IFRIO) Approx. 45 Members | | 12 Members

STEERING COMMI'I'I'EES For Major Agenda Projects

Framework for preparation and presentation of Financial Statements

• Framework provides a conceptual framework as a foundation for the preparation and appraisal of accounting standards

• FRAMEWORK is the FOUNDATION of many IFRS but is not an IFRS

• It does not have the same authority as an IFRS

• In some circumstances there may be conflict between the Framework and an IFRS. In such cases the requirements of the specific IFRS always prevail over the Framework

4

nfl

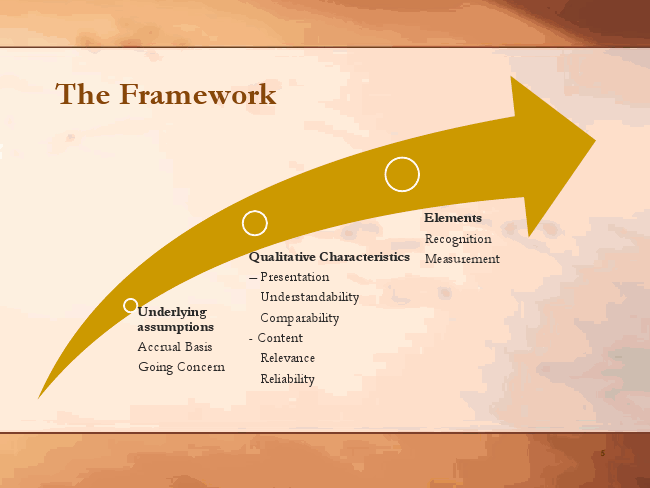

The Framework

Elements Recognition Qualitative Characteristics

Measurement – Presentation

Understandability Underlying assumptions Accrual Basis Going Concern

Comparability - Content

Relevance Reliability

5

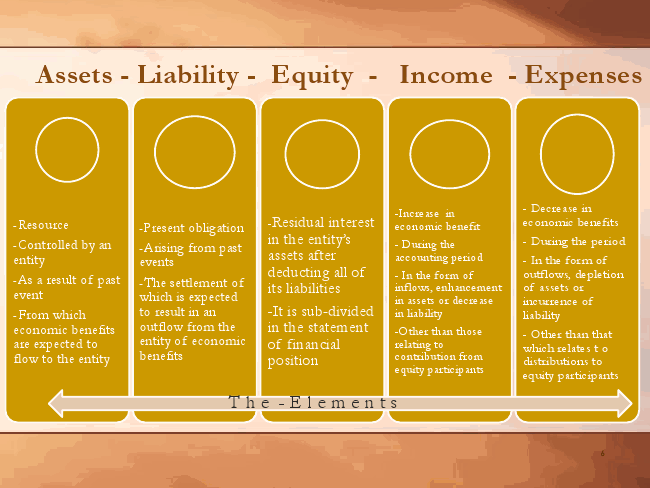

Assets - Liability - Equity - Income - Expenses

-Residual interest in the entity’s

-Increase in economic benefit

- Decrease in economic benefits

assets after deducting all of its liabilities

- During the accounting period - In the form of inflows, enhancement

- During the period - In the form of

-It is sub-divided in the statement of financial position -Resource -Controlled by an entity -As a result of past event

in assets or decrease -From which

in liability -Other than those relating to contribution from equity participants

outflows, depletion of assets or incurrence of liability economic benefits are expected to flow to the entity

-Present obligation -Arising from past events -The settlement of which is expected to result in an outflow from the entity of economic benefits

- Other than that which relates t o distributions to equity participants T h e -E l e m e n t s

6

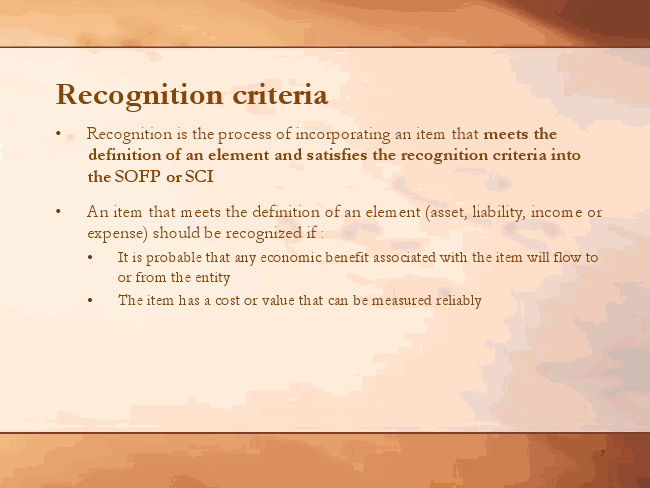

Recognition criteria

• Recognition is the process of incorporating an item that meets the definition of an element and satisfies the recognition criteria into the SOFP or SCI

• An item that meets the definition of an element (asset, liability, income or expense) should be recognized if :

• It is probable that any economic benefit associated with the item will flow to or from the entity

• The item has a cost or value that can be measured reliably

7

nfl

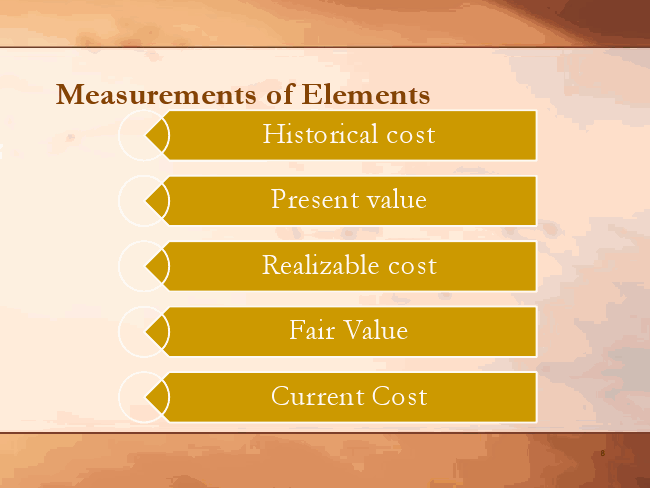

Measurements of Elements Historical cost

Present value

Realizable cost

Fair Value

Current Cost

8

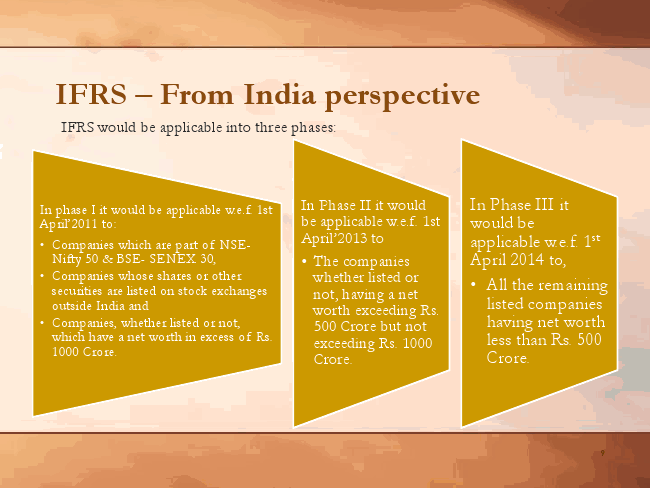

IFRS – From India perspective

IFRS would be applicable into three phases:

In Phase II it would be applicable w.e.f. 1st April’2013 to

In Phase III it would be applicable w.e.f. 1st

• The companies

April 2014 to, whether listed or not, having a net worth exceeding Rs. 500 Crore but not exceeding Rs. 1000 Crore. In phase I it would be applicable w.e.f. 1st April’2011 to:

• Companies which are part of NSE- Nifty 50 & BSE- SENEX 30,

• Companies whose shares or other securities are listed on stock exchanges outside India and

• Companies, whether listed or not,

• All the remaining listed companies having net worth which have a net worth in excess of Rs. 1000 Crore.

less than Rs. 500 Crore.

9

is

Conceptual Differences

• Substance over form

• Fair value

• Current and Non-Current Classification

• Discounting (Time value of money)

• Standards prevail over law

10