MOBU Research Report

by Pieter Vermeulen, 2018/09/04

Investment summary

In our view we consider MOBU to be a buy in the short-to medium term. Our reasons are that we see the potential that security tokens can provide in the securities market. We find that barriers to entry is high in the security tokens space and MOBU has the potential to steal the market while it has limited competitors. It has great features such as escrow that will create trust for investors and therefore grow the market.

MOBU will be limited by the growth in Bitcoin and Ethereum, which is constrained currently due to an increase in risk aversion globally, bad money that where invested and the perceived reputation after December 2017. MOBU will play a key role in Africa and specifically South Africa’s mining sector. It is our opinion that MOBU will grow at a slower rate than its management are expecting, and how it sustains these difficult stages will determine if they will survive.

We expect high volatility in MOBU price for the future and would advise that MOBU will be seen as a high risk investment and should therefore ensure that investors know this risks involved.

Business Description

MOBU is a decentralised blockchain Initial Coin Offer (ICO) platform for launching compliant security tokens. It uses ERC20 (Ethereum Request for Comments) utility token build on the Ethereum platform. What this means is that a certain set of rules need to be met before the token is accepted, which allows the blockchain asset to have value and can be send and received.

In plain languages, it is a platform for fundraising that is less costly, faster, regulated, decentralised, trades 24-hours and is based on Ethereum. Now there is a reason why there is such a hype in the market about the security coin market which will be discussed in the report.

Corporate Governance

Quality of Management

MOBU has a very complicated structure to comply with. Security coin market is still evolving and is constantly changing as it develops. The team, lead by Juan Engelbracht, has years of experience in blockchain and securities market.

Juan studied accounts Management and completed his honours. He become a stockbroker where he first saw the potential rewards available in Bitcoin when Bitcoin jumped from US$ 200 to US$ 300 in one day. He then decided to start mining Bitcoin and in 2017 started Zaber coin. This project failed and taught some expensive lessons for Juan. In my interview with Juan he said, that what they are trying to achieve, is to decrease barriers to entry for companies in the future and how they capitalize themselves. See Juans interview papers. They are trying to increase to create an environment where investors and investees can feel secure.

Paul Pelser and Braam Kruger where part of Juans team in crypto mining. Paul is an accountant and has his own accounting firm. Braam Kruger is an entrepreneur who owns a transport company, a few fueling stations and was a guest speaker with robert kiyosaki on a few occasions.

Brian Golding is Juan’s partner in Gold fund managers. Brian is the CEO of Gold Stock Brokers. One of the ten largest stock broking firms in South Africa. Brian has years of experience in securities and securities regulation environment.

Ettiene Pretorius studied with Juan and is known for being a property developer. Ettiene received entrepreneur of the year award form ABSA in 2003, one of the big five banks in South Africa.

Frikkie Van Biljon is the Chief technology officer. He started his career in 2004 as a web developer to become a systems architect and senior developer at Mukon. Frikkie is the lead JavaScript developer at Momentum.

Advisory board consists of Paresh Masani, Vladimar Nikitin and Bobir Akilhanov.

Paresh Masani is a cyber-security expert and was Vice President of Goldman Sachs and Barclays Africa with a wide technological background.

Bobir Akilhanov raised his first US$ 1 million by the age of 20 with multiple experience in startups and entrepreneurship.

Vladimr Nikitin is the legal consultant who has worked for decades in technology sector and in the ICO space. He is one of the top five ICObench certified ICO experts. He has helped raise seven successful ICOs.

Partnerships

MOBU has partnerships with few of the leading services such as:

Amazix: ICO consultancy team.

Lunalabs: ICO startup advisory company.

TOkensuite’s ICO funding.

AXIS: legal firm for the digital age.

Crypto B2B: blockchain development and outsourcing firm, Currency Analytics, a blockchain news platform.

Reputation in the market

MOBU is still a young company in the process of building a reputation behind companies like Polymath who launched in July 2017. MOBU, Polymath and TZero have the difficult task of trying to build a structure and platform that investors and investees will feel save to raise funds, generate profit and build trust.

The fact that MOBU is a startup complicates and limits its scope of investors and track record. Investors and the general public are not well informed with the team tasked in providing a platform they can trust. MOBU is reaching places such as Europe with many reporters and crypto guru’s beginning to recognise MOBU.

MOBU seems to have a good name in its currently limited market and try to inform and show to the masses that they are liabil and a worthy competitor. They do face the problem that the average person on the street find blockchain technology too complicated, despite it saying it is not. To mitigate this, it will be wise for MOBU to set up special seminars that inform the public and financial advisors how blockchain and MOBU works, the risks and return possibilities. Juan Engelbracht, CEO of MOBU, said that he would prefer to move slow and do things right. This is a good approach and only time will tell whether they will be able to stay cool-headed.

Company and industry overview

Types of Tokens

Blockchain has three types of tokens that described by the Howey test as indicated by the Security Exchange Commision (SEC). These include:

- Utility tokens - Not designed as investment, represents future access to company’s product and services, exempted from federal laws governing securities. Example: Ethereum.

- Security (Equity) tokens - Derives its value from tradable assets, subjected to federal security regulations, failure to comply to regulation could lead to penalties. Example: Blockchain Capital.

- Currency tokens - Medium of value exchange, value based on supply and demand. Example: Bitcoin.

Industry Overview

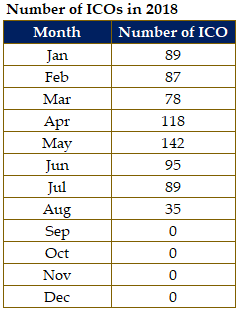

According to Business insider, Initial Coin Offerings (ICOs) raised US$ 5.6 billion in 2017 mostly driven by startups. Out of 913 attempted ICOs, 435 where successful or 48%. The average amount raised was US$ 12.7 million with 10 of the largest sales raising 25% of the total capital. This trend has continued during 2018 with decrease from June to August 2018 due to lower prices of Cryptocurrencies and investors becoming more risk averse as seen in table below.

Source: CoinSchedule, Regnum Capitis

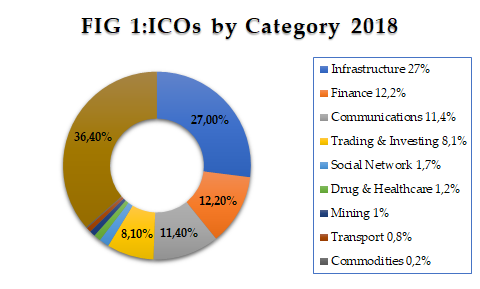

These ICOs where dominated by infrastructure, finance, communication and trading with this trend continuing in 2018 as seen in figure 1. Majority of the people that invests in these ICOs where retail and small investors. Many of these ICO’s were found to be scams where they took off with the investors’ funds. ICO Alert is one of the companies that are now trying to mitigate the widespread fraud. It is now described as “the wild west” of the investment world due to the nature of the asset trying to find class.

Source: CoinSchedule, Regnum Capitis

Institutional investors are now starting to take notice of the potential return that exists in the blockchain market. Tokens have returned 12.8 times the initial investment in dollar terms as compared to 7.7 times for Ethereum and 4.9 times in Bitcoin during 2017.

In our view, security tokens have not taken of due to regulation. Companies are afraid of hefty fines by the SEC.

Obstacles for security tokens

Launching a security token is very complicated. The nature of the security is hampered with technical, legal and regulatory obstacles. These obstacles includes:

- Regulatory headache - Globalisation has already complicated the regulatory and accounting standards. The development of blockchain complicate this process and ultimately delays the process.

- High and slow legal costs - Legal cost for launching a security token is very expensive and the process is slow. Due to the complicated nature of blockchain, consultation is required and are rare to find. The SEC fines a company if the security is issued incorrectly with a probability of jail time.

- Lack of liquidity - There are few exchanges for security tokens. Just because a company decides to tokenize its shares, does not mean that the shares can be traded. When crypto enthusiasts talk about liquidity as an advantage, they refer to the potential advantage for liquidity. When the whole ecosystem has developed, this will be an advantage versus traditional shares.

- Lack of pricing environment - The idea execution of security token idea is still new. Therefore, there are few security tokens, exchanges and demand. ICO serves providers are like startups that are still figuring out how to make it work. This is an ongoing process where nothing is set in stone and they change anything they like to survive.

MOBUs Solution

MOBU is a MRC20 utility token.

It will support Reg S, Reg D, and Reg A+ compliant security token offerings, and with the incorporated ability to select experienced legal counsel across multiple jurisdictions within the platform, token issuers can be sure they can create compliant tokens within their local jurisdictions.

MOB20 protocol will create a set of rules that govern the issuance of security tokens, and program them into smart contracts on the Ethereum blockchain so they are transparent and immutable.

MOBU will exhibit legal providers, smart contract developers, escrow providers, KNOW YOUR CLIENT (KYC) providers, etc.

MOBU will follow strict criteria for service providers in terms of track record, pricing, capital requirements, etc. This will provide transparency and an effective pricing environment.

MOBU will initiate a new standard – Know Your Supplier (KYS) for complete due diligence (DD) compliance for all service providers using the platform.

There will be a rating system for service providers which will create a competitive pricing marketplace for investors.

The Escrow agreement that MOBU has created works as follow. Company A issues a security token and gets US$ 1 million in funding from issuing the security token. The Escrow agreement limits the total amount of funding that the a company is allow the use in an attempt to protect investors from companies that issue a token and then run off with al the funding.

The company has to show what it plans to do and in that way, funds are released upon its roadmap.

MOBU will also have a lockup utility build into its utility token. The idea behind this is to limit a user from spending all of its tokens at once and in the process, create stronger demand and a higher price. The lockup period will be one year.

This special features could create trust for its investor base and fend of illegitimate companies. The drawback is that the KYC and Escrow department will have their hands full to regulate companies strategy and performance.

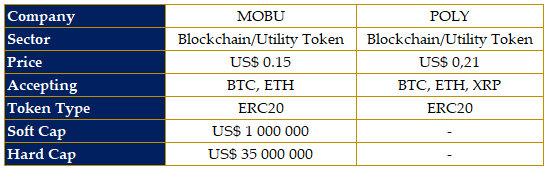

Competitive Advantage

Source: MOBU, Regnum Capitis

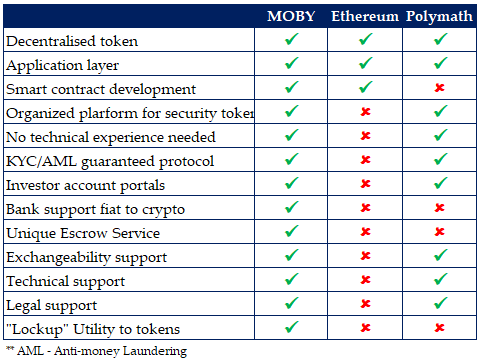

In our view, Polymath is over-capitalized compared to MOBU. It raised 58.7 million in funds. The Polymath platform works on protocols and therefore do not include rules and regulation for security tokens. It does all of the services in-house, KYC etc. This will lead to higher fees on its platform.

Company Strategy and Roadmap

Strategy and Roadmap

MOBU has a soft cap of US$ 1 million and a hard cap of US$ 50 million. What this entails is three different “game plans” that MOBU will follow.

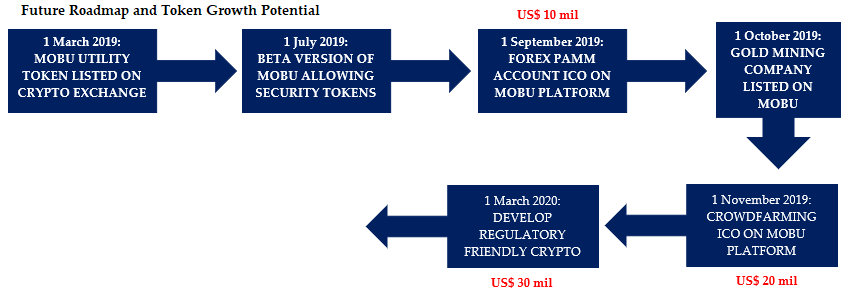

If MOBU raises US$ 10 million, it will develop the first forex and crypto PAMM (Percentage Allocation Money Management) ICO on the MOBU platform, retaining 20 percent of the autirused tokens to increase MOBU token value. The main goal of the Forex ICO is to ensure transparency.

If MOBU raises US$ 20 million, it will develop the first crowd farming ICO on the MOBU platform and retain 20 percent. MOBU platform will provide statistical data to blockchain such as what3words.

If MOBU raises US$ 30 million or more, it will develop a regulated securities exchange to ensure MOBU listed securities have a secondary market.

This is way less then Polymath with funding requirements of US$ 58.7 million. This will defer Polymath from gaining advantage above MOBU.

MOBU estimates that it will have up 350 million tokens available in total, as indicated by MOBU CEO, Juan Engelbracht. It will only list on the big exchanges and only its adviser will sell the tokens and will work through Malta or Portugal. MOBU have approached Bancor, who help AmaZix raise US$ 153 million.

MOBU will target smaller companies mainly, but not limited to South Africa. Juan indicated that they will focus on fueling stations and mines. Value of these companies range from US$ 10 to 20 million. MOBU will not focus on exchange listed companies at this stage, to sort out all its issues till the process has been redefined and automated.

We at Regnum Capitis think that it is a smart approach to start with medium size companies to build its base for the future. This will minimize losses and limit reputation risk in the long run.

A drawback is that limited amount of companies will be available on MOBU in the short run, making it harder to find quality and grow MOBU. Polymath has the upper hand in this area currently. It has identified how it will allocate companies sectors that uses the Polymath platform.

MOBU has a goal of having a thousand companies on the MOBU platform in 5-years, but in our experience we have found that startups reaches its goals in double the time. We do not think that MOBU will be an exception, mainly due to the trade-off between getting more companies on its platform and maintaining quality. The high mortality rate for these types of companies confirms our view.

Roadmap

Source: MOBU, Regnum Capitis

Source: MOBU, Regnum Capitis

Forces that drive MOBU

Confidence in traditional investments. Traditional investments are bind with red tape and vigorous regulation and performance responsibilities. This factor could lead to many investors and investees now shifting to blockchain as source of finance.

Cost of finance. Higher interest rates and high required returns could lead to companies moving to blockchain as a cheap source of finance.

Barriers to entry. The cost, legal and advisory costs of developing a security token platform is so vast that many companies could decide to rather buy existing companies to gain that function.

Price of Bitcoin and Ethereum. The price of Bitcoin and Ethereum fall dramatically from December 2017. It has since kept its downward trend with many seeing Bitcoin falling as low as US$ 1000.

Market perception of blockchain. A good image for MOBU and its investees will increase the legitimacy and demand for MOBU.

Transparency of investees information. A platform that has adequate information available will help investors to determine their risk appetite.

Liquidity. Price of MOBU tokens will increase as it controls the release of MOBU tokens and scarcity increases. Investors will therefore pay higher prices as time passes, keeping all other factors constant.

Blockchain and Ethereum specific factors. These include energy usage and cost, the media, scams and volatility of cryptocurrency.

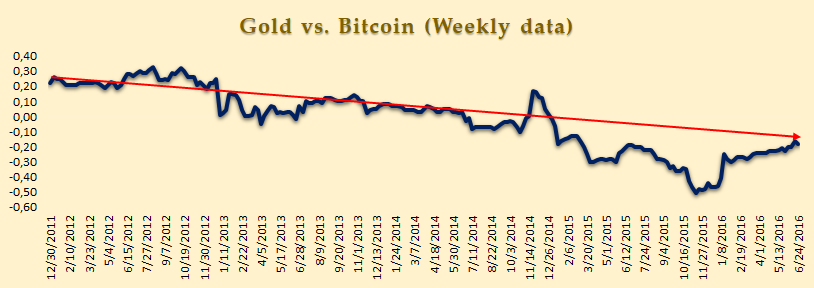

World wide risk. High risk globally will lead investors to move to saver asset classes. Gold and crypto’s seem to move in opposite direction as seen below.

Source: Bloomberg & Coindesk, Regnum Capitis.

Investment Risks and Controversies

Investment risks

Innovation and Technology. Blockchain is developing continuously as the market matures. We at Regnum Capitis believe that the market is still moving to maturity with still a lot of space for new entrants to generate adequate returns. Many investment banks are in developmental phase to create their own blockchain, based on the Ethereum and Bitcoin. These projects include IBM-backed Hyperledger Fabric project, the Utility Settlement Coin, and R3’s blockchain consortium. This is according to TechCrunch.

This will eventually drive out the smaller competitors and decrease margins or even costs that these platform charge. Investors and investors take the risk of using the MOBU platform, while a better platform is available by bigger and well capitalized banks and institutions.

Regulatory risk. The indecisiveness of regulation will hamper growth for MOBU and the blockchain space. Most countries have taken the regulate first business later - approach.

Malta on the other hand has passed 3 bills into law, establishing the first regulatory framework for blockchain, cryptocurrency and DLT (Distributed Ledger Technology).

In the United States, security tokens are governed by Rule 144 which require a holding period of 90-days for "restricted securities" of an issuer that has been a reporting company. A one-year holding period is required for "restricted securities" of a non-reporting company.

Kazakhstan have a law where you do not pay corporate taxes for the first 50-years.

The SEC recently stated that ETH and BTC are utility tokens and UKT has also mentioned that they support innovation in the cryptocurrency / fintech environment.

According to SurveyMonkey, one third of investors are against regulation and 24 percent said they trust Bitcoin more than they trust the U.S. Government. A survey was done by SurveyMonkey, which conducted a study out of a group of 5700 adults.

Reputation risk. The high percentage of scams associated with blockchain and its shortage of regulatory framework will narrow the scope of investors. The continued association with these scams and drug deals will hamper many investors from investing.

Lack of public knowledge. Blockchain sounds to complicated for the average person on the street. The 58 percent of investors in Bitcoin age from 18 to 34 years old. Out of the investor base, 71 percent is male. The biggest concern for these investors are lack of trust and opportunity for return.

Business risk. Most of the ICOs are startups with a high mortality rate of 48 percent in the first year. This is in contradiction with the stock exchange and therefore attracts and speak to a different investor base. The ICO’s are still developing its business and finding a use for their product in the market. Finding angel investors is a very difficult task and require high cost for companies and high returns to investors. According to CB Insights, only 0.91 percent of startups make it from seed stage to greater than $1 billion in value.

Smart Contract Interface

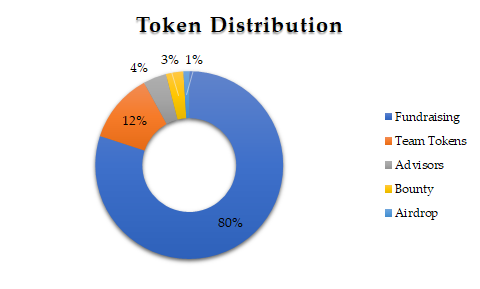

Token Distribution

Source: MOBU, Regnum Capitis

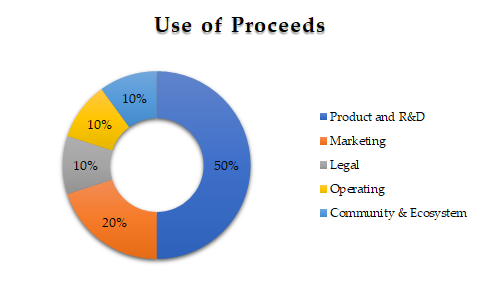

Use of Proceeds

Source: MOBU, Regnum Capitis

Disclaimer:

While we have made every attempt to ensure that the information contained in this report has been obtained from reliable sources, Regnum Capitis is not responsible for any errors or omissions, or for the results obtained from the use of this information. All information in this report is provided "as is", with no guarantee of completeness, accuracy, timeliness or of the results obtained from the use of this information, and without warranty of any kind, express or implied, including, but not limited to warranties of performance, merchantability and fitness for a particular purpose. Nothing herein shall to any extent substitute for the independent investigations and the sound technical and business judgment of the user. In no event will Regnum Capitis be liable to you or anyone else for any decision made or action taken in reliance on the information in this report or for any consequential, special or similar damages, even if advised of the possibility of such damages